{kind=link}

Shares of Philip Morris International Inc. (NYSE: PM) were down over 1% on Monday. The stock has gained 31% year-to-date. The cigarette manufacturer is scheduled to report its earnings results for the third quarter of 2025 on Tuesday, October 21, before market open. Here’s a look at what to expect from the earnings report:

Revenue

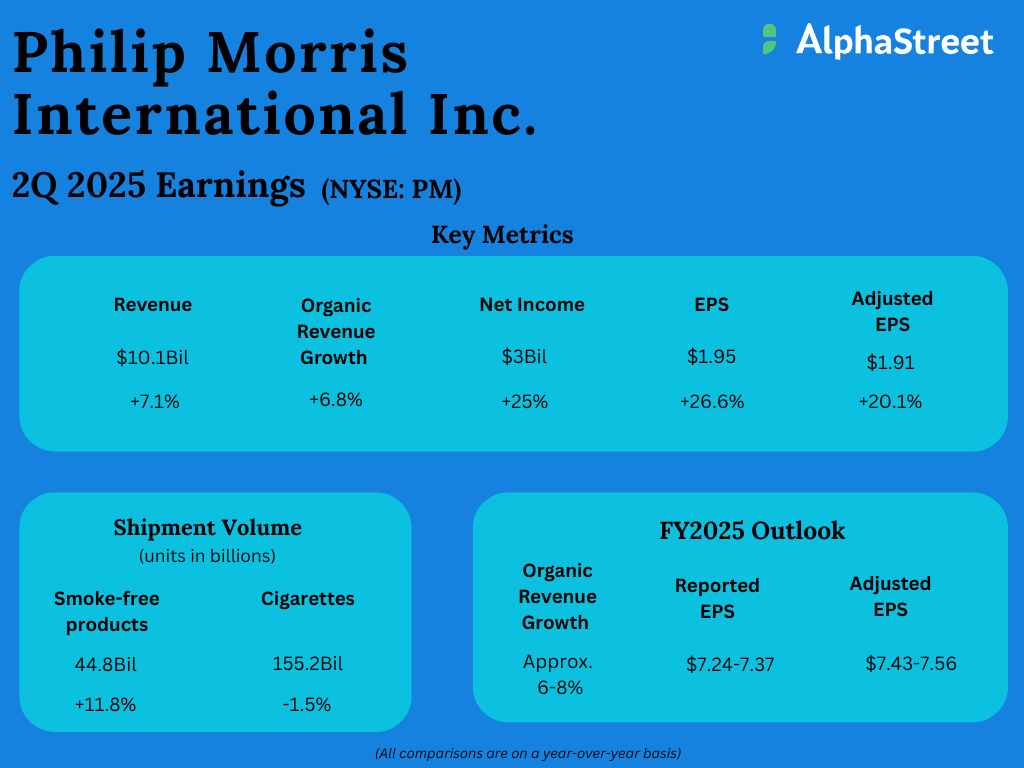

Analysts are projecting revenue of $10.66 billion for Philip Morris in the third quarter of 2025, which implies a growth of over 7% from the same period a year ago. In the second quarter of 2025, net revenues increased 7% year-over-year to $10.1 billion.

Earnings

Philip Morris has guided for adjusted earnings per share to range between $2.08-2.13 in Q3 2025. Analysts are predicting EPS of $2.10 for the quarter, which points to an increase of nearly 10% from the previous year. In Q2 2025, adjusted EPS rose 20% YoY to $1.91.

Points to note

Philip Morris is expected to benefit from continued strength in its smoke-free business, which has seen consistent growth in volumes, revenues and gross profits. This multi-category business is expected to benefit from the rising popularity of smoke-free alternatives and continued demand for smoke-free products.

In Q2, PM’s smoke-free business saw revenue growth of 15%, shipment volume growth of nearly 12%, and gross profit growth of 23%. The business accounted for 41% of total revenues and its smoke-free products are currently available in 97 markets.

The smoke-free business is led by IQOS, VEEV, and Zyn, all of which are seeing strong momentum. In its Q2 report, PM stated that IQOS exceeded $3 billion in quarterly net revenues. It continues to see strong growth in regions like Japan and Europe. In the e-vapor category, VEEV, which is currently available in 42 markets, continues to see profitable growth. In Q2, its shipment volumes more than doubled, driven by Europe.

Oral smoke-free products saw shipment volume increase by nearly 24% in Q2. Nicotine pouches saw volumes grow by 40% in the US. Zyn, which is available in 44 markets, saw Q2 can shipments grow by 43% globally. Philip Morris anticipates continued double-digit volume growth for its smoke-free products in the second half of the year, which bodes well for Q3.

PM is anticipated to benefit from resilience in its combustibles business. In Q2, despite declines in volume, combustibles saw revenues grow by over 2%, helped by strong pricing. Cigarettes volume dropped 1.5% last quarter. Meanwhile, Marlboro continues to gain market share. The combustibles business continues to see gross profit growth, which is expected to continue in the back half of the year, thereby benefiting Q3.

The post Philip Morris (PM) expected to report higher revenue and earnings for Q3 2025 first appeared on AlphaStreet.