Dune and Dusted – Farewell, Privacy Sandbox

Oct 22 2025

What’s in store

- Featured story: Dune and Dusted – Farewell, Privacy Sandbox

- Our Take On the News

- Helpful Links & Resources

Featured Story: Dune and Dusted – Farewell, Privacy Sandbox

The Bombshell That We All Kind of Expected

Last Friday, Google effectively killed the Privacy Sandbox. The company announced that it is retiring most of the APIs that constitute the broader effort, including Attribution Reporting API (Chrome and Android), IP Protection, On-Device Personalization, Private Aggregation (including Shared Storage), Protected Audience (Chrome and Android), Protected App Signals, Related Website Sets (including requestStorageAccessFor and Related Website Partition), SelectURL, SDK Runtime and Topics (Chrome and Android). Standard Chrome/Android processes will be used to phase out the technologies.

Whither the Sandbox?

The story begins back in the mists of time (2017) when Apple introduced Intelligent Tracking Prevention (ITP), a protocol limiting how long third-party cookies could be stored in the Safari browser. In March 2020, ITP was updated to block all third-party cookies by default, effectively nuking cookies from the iOS ecosystem. Shortly thereafter, in June 2020, Apple announced the App Tracking Transparency framework, which came into force with the release of iOS 14.5 in April 2021. This was effectively ‘ITP for apps’ by making iOS’s mobile ad ID (MAID) opt-in and, in effect, much scarcer. Ad tech minutiae aside, this was very effective marketing for Apple.

Why are we talking about Apple in a story that’s ostensibly about Google? Because Apple set a precedent that Google felt compelled to follow. Essentially every privacy technology that Apple announced – cookie deprecation, mobile ad ID deprecation, IP proxying – Google followed with a very similar announcement of its own. The problem is that they are very different companies: advertising is ~1% of Apple’s revenue and it has a low-single-digit share of the US ad industry, while ads represents almost 80% of Google’s revenue and the company has a ~25% market share. While Apple’s cookie and MAID policies were unhelpful to many others in the industry, the company couldn’t be credibly accused of anti-competitive behavior; Google, as the single most important player in the digital advertising industry, absolutely could. And indeed, the regulators quickly began to circle: in early 2021, the UK Competition and Markets Authority (CMA) opened an inquiry into whether removing third-party cookies in Chrome could harm competition, particularly vis-a-vis independent ad-tech vendors. Thus commenced a long and awkward dance between Google and privacy regulators, marked by numerous technical changes and deadlines pushed back and pushed back again. Many publishers and vendors shifted focus to first-party data and alternative IDs, and active testing of Sandbox proposals dwindled.

Waving the White Flag

The browser-API approach struggled to meet advertiser utility and adoption thresholds. Google’s own postmortem cites low adoption and feedback on limited value as key reasons to retire the APIs.

Just as important would seem to be Google’s wider considerations vis-a-vis government regulators around the world and the ongoing threats to its ad tech business. Consider the legal gauntlet the company has run of late: a federal judge found that the company maintained an illegal search monopoly, and only escaped severe remedies by the stroke of luck that LLMs have recently begun contesting the search market; in a separate case, a different federal judge found that the company monopolized multiple markets and illegally tied its publisher ad server to its ad exchange. Remedies have not yet been determined in the latter case, though compelled divestitures of pieces of Google’s ad tech stack are thought to be in play.

Against this backdrop, Google would be seriously tempting fate (read: regulators and judges) by plowing ahead with its Privacy Sandbox plans. As we’ve said before, privacy and competition are in insoluble tension; Google and other tech majors cannot offer users systematically greater privacy without diminishing competition in the industry. For evidence, look no further than GDPR, which sought user privacy but ended up entrenching the dominance of Google and Meta in Europe.

What Happens Now

With cookies persisting in Chrome and the GAID likely persisting in Android, it looks like we will avoid another ‘ATT recession.’ Apple’s App Tracking Transparency rollout in 2021 is instructive: by removing a critical ingredient used in measurement and targeting, the policy change harmed platforms and advertisers (especially small businesses) by making it more difficult to serve ads to qualified and interested consumers. But in the longer run, IDFA deprecation deepened Meta’s moat: none of its peers had the scale of user interactions, event volume, on-device signals, and AI/ML investment to rebuild end-to-end probabilistic systems and conversion modeling. Google’s Sandbox decision, by implication, means other ad tech players can remain viable and maintain healthy levels of competition.

Finally and most importantly, what does this mean for you? We would highlight:

- Keep optimizing around existing cookie and especially MAID rails

- Test FedCM for sign-in flows and CHIPS for service isolation without cross-site tracking

- Double down on first-party data and consented identity

- Watch the W3C interoperable attribution effort as the likely standards-based path for privacy-preserving measurement (we will of course keep you fully informed)

And of course maintain contingency plans for further policy shifts, because the privacy/competition pendulum can swing again. | Privacy Sandbox, MDM, Digiday, AdExchanger

What We’re Tracking

The news stories we’re tracking that are likely to impact advertisers in the month ahead.

U.S. Economy

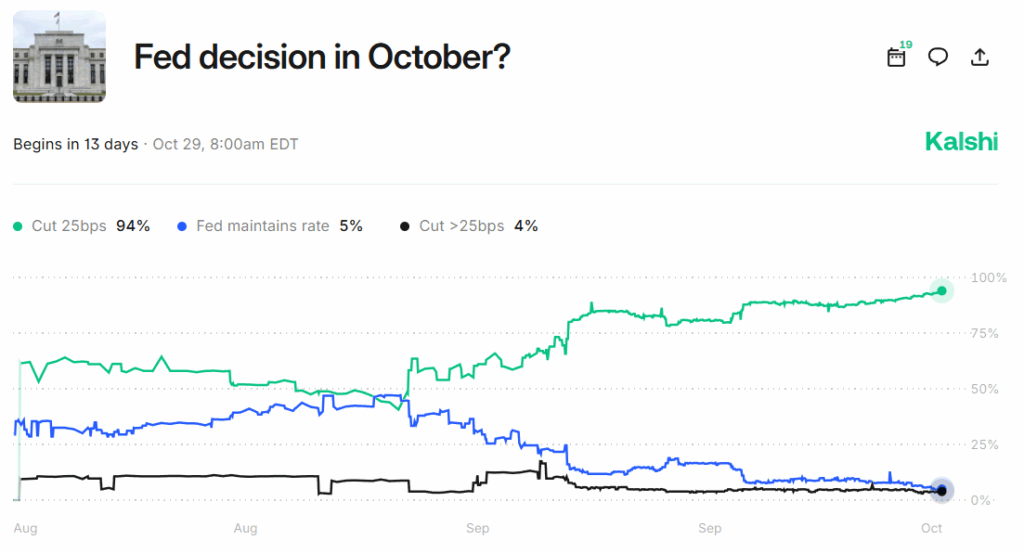

1. According to consumer credit card data, consumer spending growth moderated in September as consumers express declining sentiment and face a weakening labor market. Spending patterns may also be inhibited by consumers’ rising expectations for inflation.

While the federal government remains shut down we don’t have official employment data, but the private equity firm Carlyle Group has published its own employment index which estimates net job creation in September of 17,000, which would be one of the weakest job creation months since the 2020 recession. While the data are of course unofficial, they are consistent with other measures indicating significant cooling in the labor market. Employment is of course one component of the Federal Reserve’s dual mandate, and it is concerns about the labor market that are driving the strong likelihood of rate cuts in October. | Bloomberg, Bloomberg

2. Astute readers may recall that, back in April, we flagged plans from the US Trade Representative to impose new and significant port fees on Chinese-built vessels; this is an additional, non-tariff measure in the Administration’s ongoing trade war with China. These plans came into force on Tuesday the 14th – the US is now imposing port fees of $50 per net ton for Chinese vessels, and the greater of $18 per net ton and $120 per container for non-Chinese operators of Chinese-built vessels. To give some sense of proportion, modern ocean freighters might carry 150,000 net tons of cargo with a merchandise value of ~$1 billion. The new fees will add $7.5 million, or just under 1% of merchandise value, to the cost of transporting goods to the US; the $50 fee is scheduled to rise to $140 by 2028.

As with tariffs, retaliation is a risk, and indeed the Chinese government has said it will impose new fees on US ships docking in China. The ostensible motivation for the new fees is to revitalize American shipbuilding, which has withered to almost nothing:

Critics contend that state protection is actually the cause of our decline – the Merchant Marine Act of 1920, better known as the Jones Act, has restricted water transportation of cargo between US ports to ships that are US-owned, US-crewed, US-registered, and US-built; you can see the results above. The net effect has been much heavier road-based goods transportation and disuse of the US’s highly navigable waterways. Nevertheless, there is proposed bipartisan legislation in Congress to provide new subsidies to the US shipping industry. | NYT

Tech Giants & Platforms

1. Meta is poised to gain share of US social ad spending for the first time since 2018, owing to its strengths in AI-driven ad optimization, creative automation, and click-to-message formats. Meta will net about 69% of US social spending this year, miles ahead of second-placed TikTok at about 12%.

The other big social story is Reddit, which has more than doubled its ads business since 2023 and will grow ~56% this year, surpassing X in terms of advertising revenues. | eMarketer

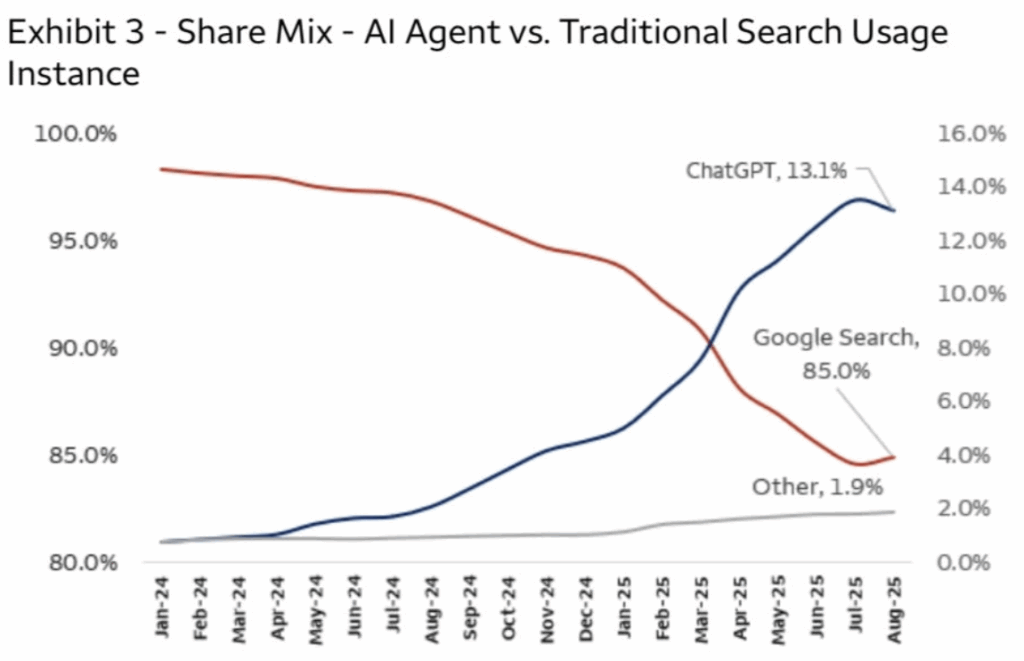

2. A recent Wells Fargo research report caused a bit of a stir by claiming that Google’s Gemini has begun to claw back search share from ChatGPT:

This generated some pushback, as people pointed out that Google search share is still down substantially from early 2024:

Two things seem undeniable at this point. First, Gemini has overcome its early adoption struggles and has gained major momentum, partly catalyzed by its Nano Banana moment:

Second, ChatGPT is the consumer AI behemoth and, while it no longer has the chatbot market to itself, shows no signs of slowing down.

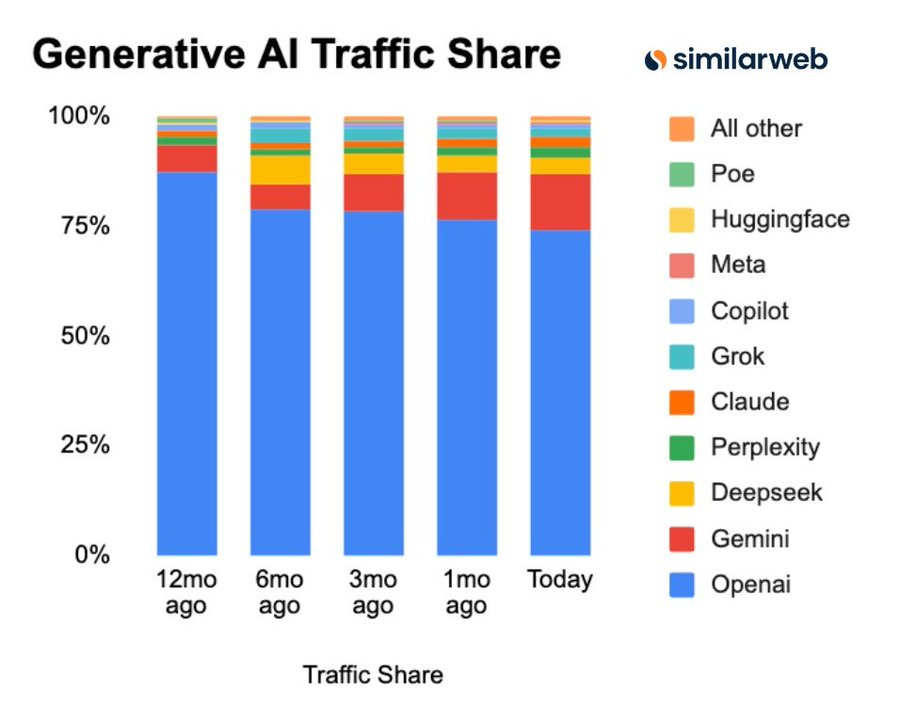

It recently disclosed that it has hit 800m weekly active users, up from 700m in August and 500m at the end of March. And it’s not just ChatGPT – in case you missed it above, OpenAI now has multiple products leading the App Store. | @StockMarketNerd, @Similarweb

Media & Advertising

1. Prepare yourselves, racing fans … for a new streaming subscription. Formula 1 announced on Friday that Apple will become the sport’s exclusive US broadcast partner as of the 2026 season. The rights will transfer from ESPN, which has held them since 2018 in a deal worth $90 million per year; it’s been reported that Apple will pay $120m – $150m per year for the new rights package.

From F1’s perspective, the deal with Apple is not only a superior financial outcome, it also furthers its goal to be “part of the culture” in the US – to that end, Apple will not only air all on-track action on its streaming platform, but will also “amplify the sport across Apple News, Apple Maps, Apple Music, Apple Sports, and Apple Fitness+.” From Apple’s perspective, it is part of a platform reboot: despite its content being widely lauded for quality, its share of the streaming market is abysmal, well below even the second- and third-tier streamers. The F1 deal, following on the heels of the very successful Apple Original F1: The Movie, doubles down on a new, sports-and-culture-centric strategy.

This deal is not without its risks, however – look no further than Major League Soccer for a cautionary tale. In 2022, its last year on ESPN, MLS averaged 343k viewers per game; two-and-a-half years into its exclusive ten-year deal with Apple TV, the MLS Season Pass service is averaging 120k viewers per game, a two-thirds decline in 30 months. Back in 2022, MLS was a burgeoning league, with a small but growing fanbase, trying to crack the extremely crowded American sports market; putting it behind Apple’s paywall seems to have killed that momentum. Formula 1 must learn from MLS’s experience, and learn fast – there are only about 140 days until the opening race weekend of the 2026 season. | @F1Media, The Athletic

2. Netflix has expanded its gaming initiatives to the biggest screen in the house. In case you missed it, Netflix has offered videogames as part of the subscription package for four years, but users could only play those games on mobile devices. Now, subscribers will be able to play games on their TV screens, using their phones as controllers. Netflix is prioritizing social games that can be played in groups, offering titles like Boggle Party, Pictionary: Game Night, and Lego Party.

While gaming might seem somewhat orthogonal to Netflix’s core business of developing and licensing shows and films, the company has long viewed its business as a mission to capture more of users’ finite time; founder and former CEO Reed Hastings famously said Netflix’s real competition is sleep. The objectives here are to give customers more reasons to spend more time in the Netflix ecosystem, which increases the opportunity to monetize that time through ads; reduces churn (if canceling means losing not just shows, but games as well); and allows the company to amortize the fixed costs of content production over even more user minutes. | Bloomberg

Helpful Links & Resources

- WarnerBros Discovery has rejected an acquisition proposal from Paramount Skydance as “too low”; expect another bid soon

- Apple has quietly rebranded its streaming service, removing the ‘+’ to become simply ‘Apple TV’

- Spotify and Netflix are forming an anti-YouTube alliance with a partnership bringing Spotify podcasts exclusively to Netflix’s video platform

- Spotify is also launching a FAST (free ad-supported TV) channel with Samsung TV Plus

- Walmart is taking a high-variance bet that partnering with OpenAI will supercharge ecommerce without cannibalizing its high-margin ad business

- Mobile ad network AppLovin has shuttered a key product that was allegedly enabling downloads to user devices without consent

- Cancellation rates for both Disney+ and Hulu doubled in September following Disney’s suspension of ‘Jimmy Kimmel Live!’

You Might Be Interested In