{kind=link}

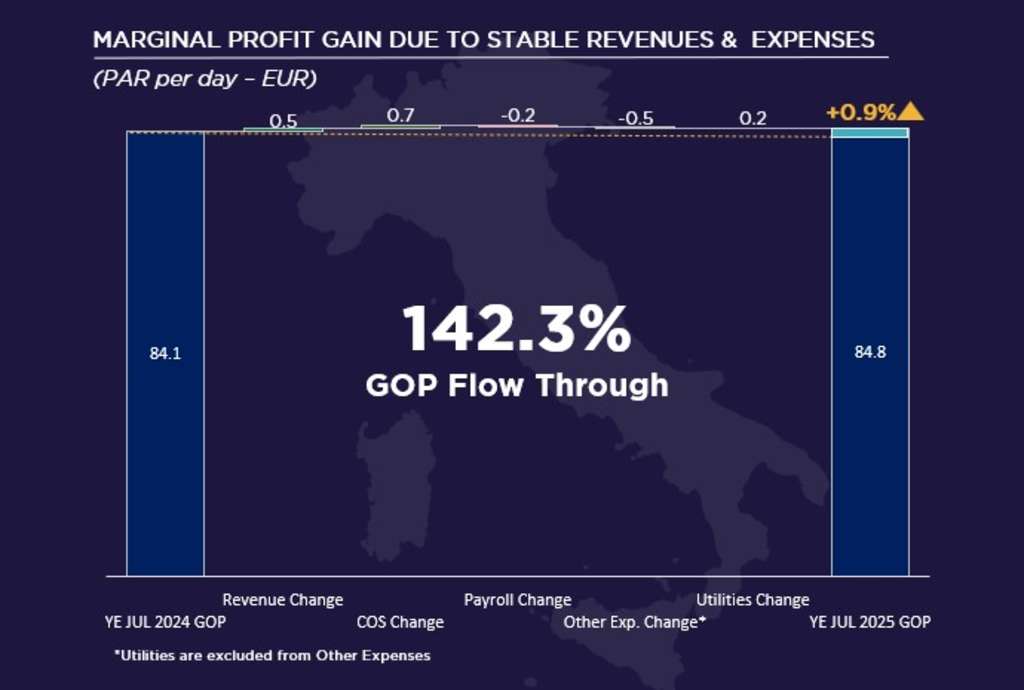

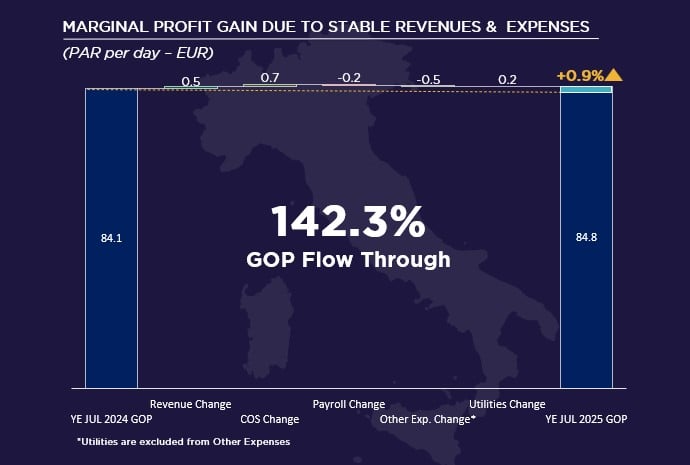

The sample of branded full-service hotels* in Milan recorded a slight increase in profit during the 12 months ending in July 2025, compared to the same period last year. GOP per Available Room (GOP PAR) rose by 0.9%, driven by a 0.2% increase in revenue and supported by a 0.2% decrease in expenses.

OVERVIEW

- The sample of branded full-service hotels* in Milan recorded a slight increase in profit during the 12 months ending in July 2025, compared to the same period last year. GOP per Available Room (GOP PAR) rose by 0.9%, driven by a 0.2% increase in revenue and supported by a 0.2% decrease in expenses.

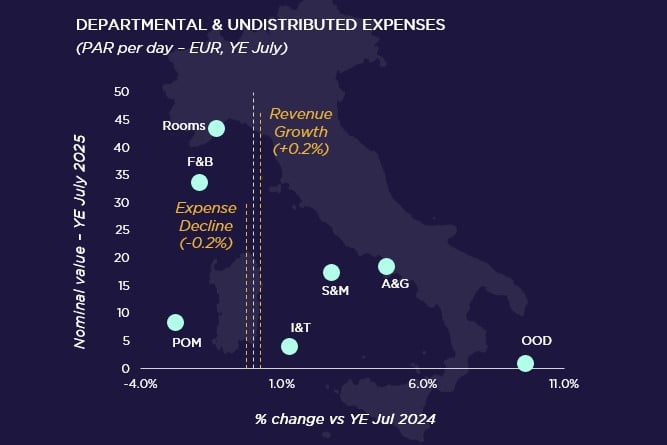

- The revenue growth was driven by the Rooms department (+0.9%) as ADR increased by 2.2%, reaching €250, compensating for the -1.3% occupancy decline to 68.4%.

- F&B revenue declined to €44.3 PAR (-0.7%), albeit less than occupancy, resulting in increasing F&B revenue per occupied room (+0.6%), reaching €64.7 (POR).

- The decline in expenses was driven by Cost of Sales (-€0.7 PAR) and Utilities (-€0.2 PAR).

- Occupancy rates dipped primarily in August (-14.9%), September (-13.4%) and October (-7.6%) (YoY). Conversely, hotels recorded +10%, +4.5%, and +5% increases in February, April, and May 2025.

- The occupancy pressure was partially caused by the opening of 11 hotels during the past 12 months (+616 rooms) and one closure (62 rooms). However, as the additional rooms represented only a +0.9% increase in annual supply (YoY), the impact was limited.

- Overall, due to the declining expenses, 142% of the revenue increase flowed through to the bottom line (GOP). The profit margin improved by 0.2pp, reaching 38.8%.

*Quality hotels in the city – excluding luxury properties

SUPPLY

- Over the last 12 months (YE July 2025), the Milan hotel market recorded 11 hotel openings (+616 rooms), including 10 new hotels (536 rooms) and the re-opening of Casati 18 hotel (80 rooms) in July 2025, following a complete renovation.

- The new openings were partially offset by the closure of Hotel Scala (-62 rooms), with a potential reopening in 2027.

- Overall, the hotel supply in Milan increased by +0.9%, compared to the same period last year (weighted by opening and closing dates).

- The majority of the new room supply was within the full-service sector, with Luxury Class hotels representing 42.9%, followed by the Upscale properties accounting for 30.3%.

- Most of the new hotel supply (74%) opened in the city centre of Milan between the historical part of the town and the Centrale Railway Station neighbourhood.

- Furthermore, the Four Seasons (118 rooms) underwent a full renovation throughout the year without fully closing.

- Going forward, the New Rocco Forte Hotel is expected to open in the city center in November 2025 (71 rooms).

PAYROLL COSTS

- The labor expenses decreased by 0.2%,reaching €61.4 PAR during YE July 2025. The F&B department led the decline, where payroll dropped by €0.5 PAR (-2.2%), while the labour costs in the A&G department recorded the most notable increase (+€0.4 PAR, +4.7%).

OTHER EXPENSES (excl. Utilities)

- Other expenses remained relatively stable, recording a minor €0.5 PAR increase (+1.1%) to €46.3 PAR. The departments mostly contributing to this overall increase were S&M (+€0.5 PAR) and A&G (+€0.4 PAR).

COST OF SALES

- Total Cost of Sales decreased by €0.7 PAR (-3.8%), primarily in the Rooms (-€0.6 PAR) department.

UTILITY COSTS

- Utility costs decreased by €0.2PAR (-1.9%), driven by a reduction in electricity expenses (-€0.4 PAR).