{kind=link}

Housing security is something I hope everyone will one day obtain. Once you are house secure, you can more easily focus on your career, family formation, and other things you care about. However, if you rent for life, you may face housing insecurity, which can feel especially uncomfortable when you’re older or no longer willing or able to work.

Of course, I understand why some people argue against homeownership. They say it’s a poor investment, a hassle, and ties you down. I get it.

But many of those who are anti-homeownership have also missed out on tremendous property price appreciation over the years. Most have been renters their entire lives, whereas I’ve been both a renter and a homeowner. I’ve also made and lost money from real estate. Still, I believe homeownership is the path to building wealth for most people.

Real estate FOMO is just as powerful as investing FOMO. But as you crusade against homeownership, try to remember the average person – someone who values stability, may want to start a family, and isn’t making a fortune selling courses or building an online empire.

As a savvy investor, you want to invest in assets that outpace inflation over time. Housing is one of those assets.

Fix Your Living Costs Sooner, Rather Than Later

To help you build more wealth, your goal should be to fix your living costs as much as possible because inflation is too powerful of a force to overcome. And if you eventually become a landlord, the combination of rising rents and property prices will likely build you a tremendous amount of wealth over time.

Conversely, as a renter, you are effectively short the housing market. The only way you truly benefit is if rents and property prices decline. While they do drop during every cycle, the long-term trend is undeniably up due to the chronic undersupply of housing and a growing population.

Just as it’s unwise to short the S&P 500 over the long run, it’s also unwise to short the real estate market indefinitely by renting. Time and inflation tend to work in favor of the owner, not the renter.

The government also provides multiple tax incentives for homeownership — from the mortgage interest deduction to depreciation to the $250,000/$500,000 in tax-free capital gains if you sell. Through consistent forced savings, you’ll gradually build equity and free up cash flow to invest in other risk assets like stocks, if you wish.

A Difficult Situation With Rising Rents in NYC

Let me share a situation that reinforces why I don’t recommend renting indefinitely. It’s based on my experience helping a relative manage her finances – something I did for free and, in hindsight, carried emotional costs of its own.

I’m witnessing the effects of housing insecurity firsthand, even for someone with a seven-figure investment portfolio, partially because of decades spent renting.

For privacy, I’ve changed all of the details. However, the ratios and percentages are the same.

Year-End Financial Review Time

Whenever I conduct a financial review, I don’t just look at investments. That’s only one part of the equation. To truly help someone, you have to understand their objectives, expenses, retirement timeline, and life plans. You can’t set financial goals without knowing what’s going out the door each month.

My relative has lived in New York City for about 32 years. But she’s been feeling tremendous cost-of-living pressure because her $3,800-a-month two-bedroom apartment has become unaffordable given she only earns about $30,000-a-year as a substitute teacher and other part-time jobs. The only way she can cover rent is by drawing down from her investments.

At the beginning of the year, she asked whether she should move to a smaller apartment in a less desirable area to save. Normally, I would have said yes. But because she had around $1.63 million in various investments (IRA, Roth, Taxable), $800,000 of which was taxable, I told her to stay put for now. At 55, she deserved some stability after multiple moves, including leaving Manhattan to Queens to save money.

Based on my relatively positive market at the beginning of the year, I felt her 60/40 portfolio, which I constructed with low-cost ETFs, could sustain her lifestyle for a while longer. Thankfully, 2025 turned out to be another strong year for the markets.

Now the Landlord Is Aggressively Raised the Rent

Unfortunately, she just got notice her landlord will hike her rent next year from $3,800 to $5,200 a month. That increase pushes her annual expenses from roughly $80,000 to about $100,000, factoring in inflation across other categories as well.

On the surface, spending $80,000 a year when your income is only $30,000 gross is excessive. However, she’s been working, saving, and investing diligently for more than 30 years. And as we age, most of us want to maintain or even improve our standard of living, not cut back.

Based on her net worth and my market outlook at the beginning of the year, I believed maintaining her lifestyle was reasonable for one more year. To be frank, I also didn’t have the heart to tell her to downshift her lifestyle at her age. She has the net worth at her age.

Still, the math tells a tougher story.

To sustainably support ~$100,000 in annual spending, you generally need between $2 million and $2.5 million invested, assuming a 4%–5% withdrawal rate. She’s close, at ~$1.8 million total with $880,000 in a taxable portfolio to draw from, but not quite there.

And while the numbers might suggest she could make it work, the emotional reality is very different. It’s incredibly hard to withdraw $8,000–$10,000 a month from your portfolio and watching your balance slowly decline. One 10% correction and such a withdrawal amount would feel impossible.

Get a Higher Paying Job or Downgrade Your Lifestyle

The rational solution is clear: cut expenses and boost income. Unfortunately, finding a higher-paying job at age 55 in a competitive, age-sensitive job market is difficult. She had been out of the workforce for years as a stay at home mom.

At least, for one more year, she managed to enjoy a lifestyle that her finances didn’t fully justify, thanks to a roughly 10% portfolio gain. It was a risk we took at the beginning of 2025, that has paid off. But the grace period is over. With a 35% rent increase looming and the S&P 500 trading at 23X forward earnings, it’s time to downgrade.

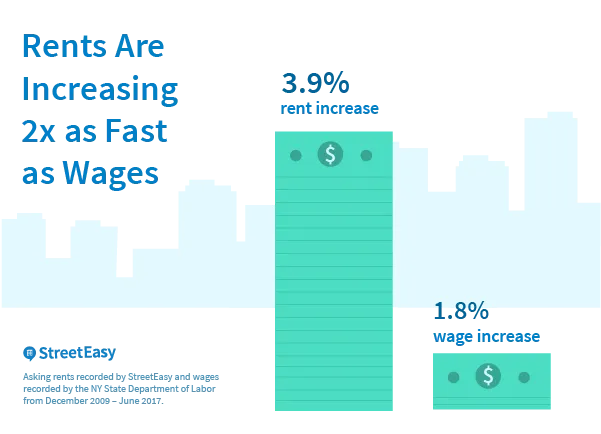

This is the sad reality of lifelong renting. Over time, rents tend to rise faster than wages and inflation. Eventually, you get squeezed hard enough that you have to move — sometimes far away from the community you’ve built.

Greater Peace of Mind with Homeownership

When you own your home, you fix roughly 85% – 90% of your living expenses for as long as you own it. You’re no longer at the mercy of your landlord raising rent or selling the property. You have housing security – a form of peace that becomes increasingly valuable as you age and your career energy wanes.

Because let’s be honest: as you get older, your desire and ability to grind for income decline. If you take time out of the workforce – for parenting, caregiving, or simply burnout – it can be hard to find another well-paying job later on.

Owning your home eliminates that uncertainty. It’s a financial and emotional anchor.

Below is a sad yet fascinating chart showing the rising median age of U.S. homebuyers. For first-time buyers, the median age is now 40.

You could argue this reflects worsening housing affordability as renters are being forced to save longer before they can buy. But you could just as easily argue that this trend underscores the value of homeownership, given how much housing has appreciated over time.

After more than 45 years of the median homebuyer age steadily increasing, do we really think this trend will reverse anytime soon? Unlikely. Demand continues to outpace supply, and more foreign real estate buyers are scooping up what still looks like inexpensive U.S. real estate compared to their home markets.

Just look at what has happened in Canada, where the government openly allowed foreign buyers to purchase real estate, sometimes with illicit funds, for decades. As a result, foreigners helped drive prices to levels that became unaffordable for many local citizens.

When there are massive financial incentives at play, it’s hard for some politicians to do the right thing. Eventually, if you don’t see the value in owning U.S. property, someone else will. Do not rely on power-hungry try politicians to help you.

Please Don’t Rent Forever If You Don’t Have To

My relative could have bought a two-bedroom condo 8–10 years ago. I wish we would have had a financial consultation back then. She chose the flexibility of renting instead. Had she purchased back then, her monthly housing costs would now be relatively fixed, and her condo would likely be worth 20%–40% more. Not a fantastic return compared to the S&P 500, but a great trade-off for stability plus appreciation on a large asset.

If you know where you want to live for at least five years — ideally 10 — buy instead of rent. Inflation is simply too powerful to combat indefinitely, and rent increases don’t stop for anyone.

Perhaps if housing costs continue to soar, new political leadership will step in with more effective solutions. But I wouldn’t count on it. Depending on the government to save you is an unstable strategy. Depending on yourself, on the other hand, is the foundation of financial freedom.

In the end, owning your home isn’t just about money. It’s about peace, dignity, and control of your life. And if you can secure that for yourself, your family, and your future, why wouldn’t you?

Build Your Castle While You Can

Life is unpredictable, and we all face different financial and personal challenges. But the one thing we can control is how much we depend on others for our basic needs. Shelter is foundational. Once you secure it, everything else—career, family, purpose—becomes easier to manage.

Whether you choose to rent or buy, the key is to make a conscious, numbers-based decision. Just know that, ironically, the longer you rent, the harder it becomes to break free.

Here are five actionable steps to move closer to housing security:

1) Run your rent vs. buy numbers every year.

Don’t rely on old assumptions. Plug your rent, income, and local home prices into a calculator to see where the crossover point lies. When rent inflation is factored in, ownership often wins sooner than expected.

2) Think in decades, not months.

If you plan to stay put for at least five years, buying usually makes sense. Real estate rewards time and patience, not market timing.

3) Save aggressively for a down payment.

Treat your down payment fund like an investment in freedom. Even if you don’t buy right away, that savings cushion builds optionality and discipline.

4) Buy what you can comfortably afford.

You don’t need your dream home right out of the gate. A modest, well-located property that keeps your monthly expenses stable is often the best wealth builder. Please follow my 30/30/3 rule for home buying.

5) Don’t rely on luck, politicians, or anyone else.

Markets shift. Policies change. Promises fade as politicians promise the world to get into power. But owning your home gives you control over one of life’s biggest variables—your cost of living. It’s a personal hedge against uncertainty.

Bottom line: If you can buy and hold for the long term, do it. Renters must constantly adapt to the market, while homeowners eventually let the market adapt around them.

Build your castle while you can, because once you do, you’ll have the foundation to live the life you truly want.

Readers, what are your thoughts on renting for life? If you’ve been a lifelong renter, do you believe you’ve built more wealth than if you had purchased a primary residence? Have you ever been forced to move because your landlord imposed an aggressive rent hike? And why do you think some people who’ve never owned a home are so strongly against homeownership when there is so much data showing the median net worth of a homeowner is far greater?

Invest In Real Estate Passively

If you can’t buy a home yet, don’t sit on the sidelines while housing prices and rents keep rising. You can still participate in the real estate market and build wealth over time — without needing to come up with a massive down payment.

That’s why I’ve invested with Fundrise, a platform that allows everyday investors to gain exposure to residential and industrial properties nationwide. With over $3 billion in assets under management and 350,000+ investors, Fundrise makes it easy to own a piece of the real estate market that continues to compound in value.

Real estate has historically been one of the best ways to hedge against inflation and grow wealth passively. And with a minimum investment of only $10, anyone can start investing today.

Fundrise has been a long-time sponsor of Financial Samurai because our philosophies align — consistent, disciplined investing in tangible assets to build financial freedom.