{kind=link}

Housing prices in parts of New Mexico are flashing warning signs—and fast. According to data from the Zillow Home Value Index, 18 towns across the state show patterns that often come before a crash: sudden surges, extreme volatility, and unsustainable growth above long-term trends.

Our deep dive into 15 years of price data uncovered towns that have crashed before—and are now showing familiar signs of overreach. Whether it’s price whiplash, too-fast momentum, or values that simply don’t pencil out, these places could be headed for a hard reset.

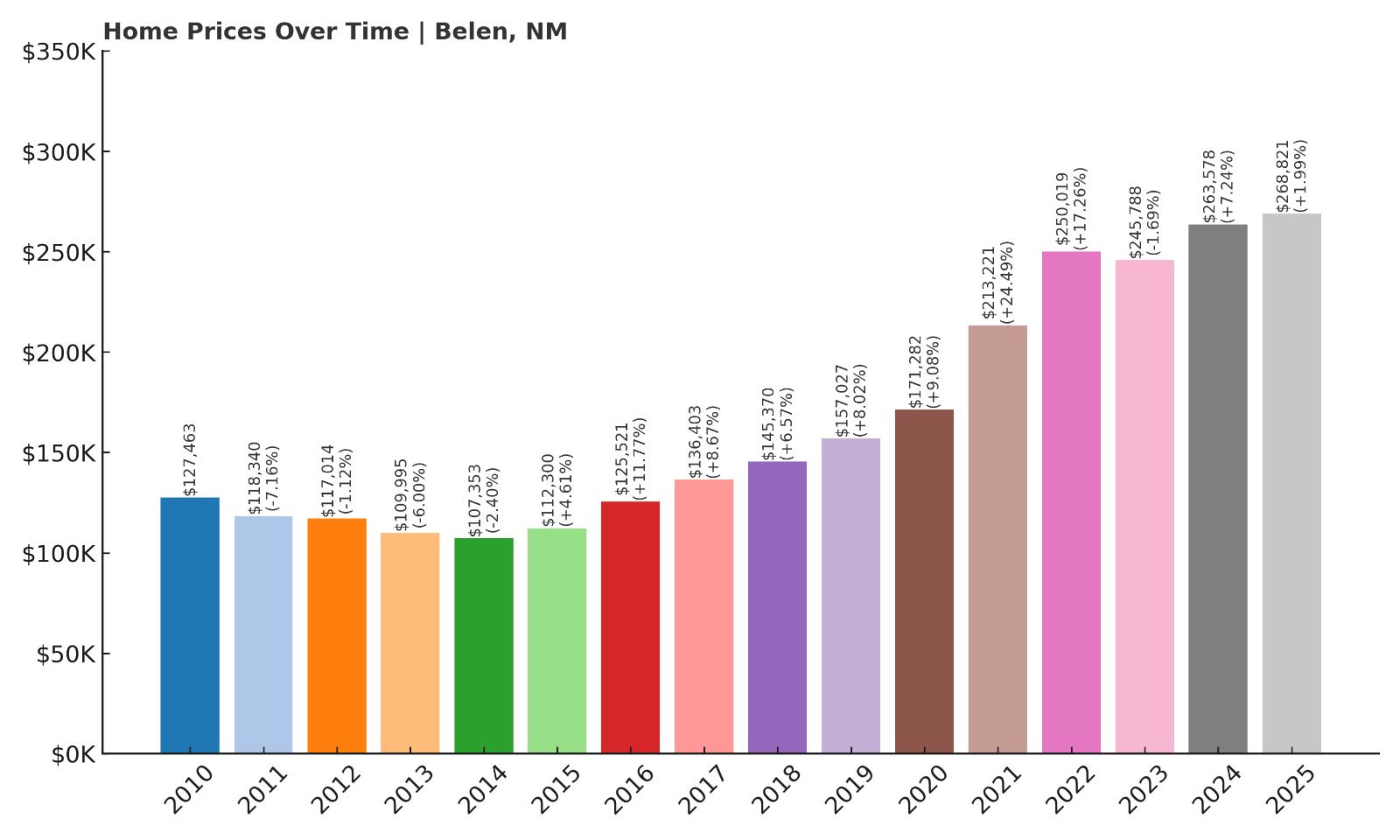

18. Belen – Crash Risk Percentage: 54.95%

- Crash Risk Percentage: 54.95%

- Historical crashes (8%+ drops): 2

- Worst historical crash: -7.2% (2011)

- Total price increase since 2010: 150.4%

- Overextended above long-term average: 61.1%

- Price volatility (annual swings): 8.6%

- Current 2025 price: $268,821

Belen’s housing market shows concerning signs of overheating, with home values climbing 150% since 2010 and currently sitting 61% above the long-term average. The city has already experienced two significant price drops, including a 7.2% crash in 2011 that followed the national housing crisis. With annual price swings averaging 8.6%, Belen demonstrates the kind of volatility that often precedes major corrections.

Belen – Dangerous Overextension After Massive Growth

Located 35 miles south of Albuquerque along the Rio Grande, Belen serves as a transportation hub with significant rail infrastructure that has historically supported its economy. The city’s housing market surged dramatically over the past 15 years, with median home prices more than doubling from $127,463 in 2010 to $268,821 today. This explosive growth has pushed values far beyond sustainable levels, creating conditions ripe for a sharp correction.

The warning signs are particularly stark when examining recent price patterns. After reaching $250,019 in 2022, prices dipped slightly before rebounding, a classic pattern of market uncertainty. With homes now priced 61% above their historical trend line, Belen faces mathematical challenges in sustaining current values. The combination of overextension, historical volatility, and previous crash experience places this Valencia County community at significant risk for the next housing downturn.

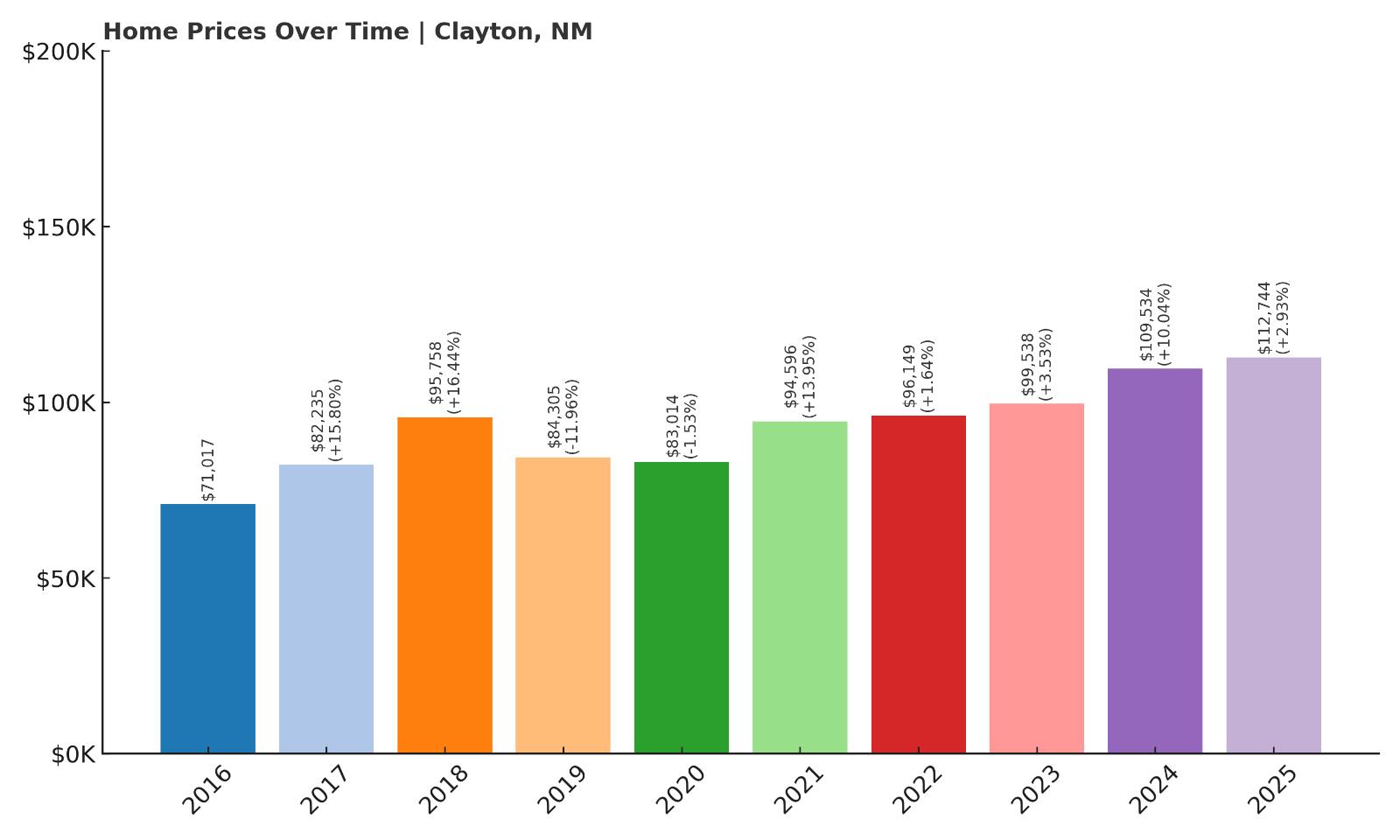

17. Clayton – Crash Risk Percentage: 55.45%

- Crash Risk Percentage: 55.45%

- Historical crashes (8%+ drops): 1

- Worst historical crash: -12.0% (2019)

- Total price increase since 2016: 58.8%

- Overextended above long-term average: 21.4%

- Price volatility (annual swings): 9.3%

- Current 2025 price: $112,744

Clayton’s housing market demonstrates concerning instability with a severe 12% crash in 2019 and high annual volatility of 9.3%. Despite recovering from that crash, home values remain 21% above long-term trends and have risen nearly 59% since 2016. The combination of recent crash history and continued overextension signals potential vulnerability to another downturn.

Clayton – Recent Crash History Raises Red Flags

This Union County seat near the Colorado and Oklahoma borders has historically relied on agriculture and energy sectors, creating an economy sensitive to commodity price fluctuations. Clayton’s housing market reflects this underlying volatility, with the dramatic 12% price crash in 2019 serving as a stark reminder of how quickly values can collapse. The crash dropped home prices from $95,758 to $84,305, wiping out years of gains in a single year.

While prices have recovered and even exceeded pre-crash levels, reaching $112,744 in 2025, the rapid 59% increase since 2016 has pushed the market into overextended territory once again. Clayton’s remote location and dependence on volatile industries make it particularly susceptible to economic shocks that could trigger another significant price correction. The town’s proven ability to crash quickly, combined with current overvaluation, creates a dangerous setup for homeowners.

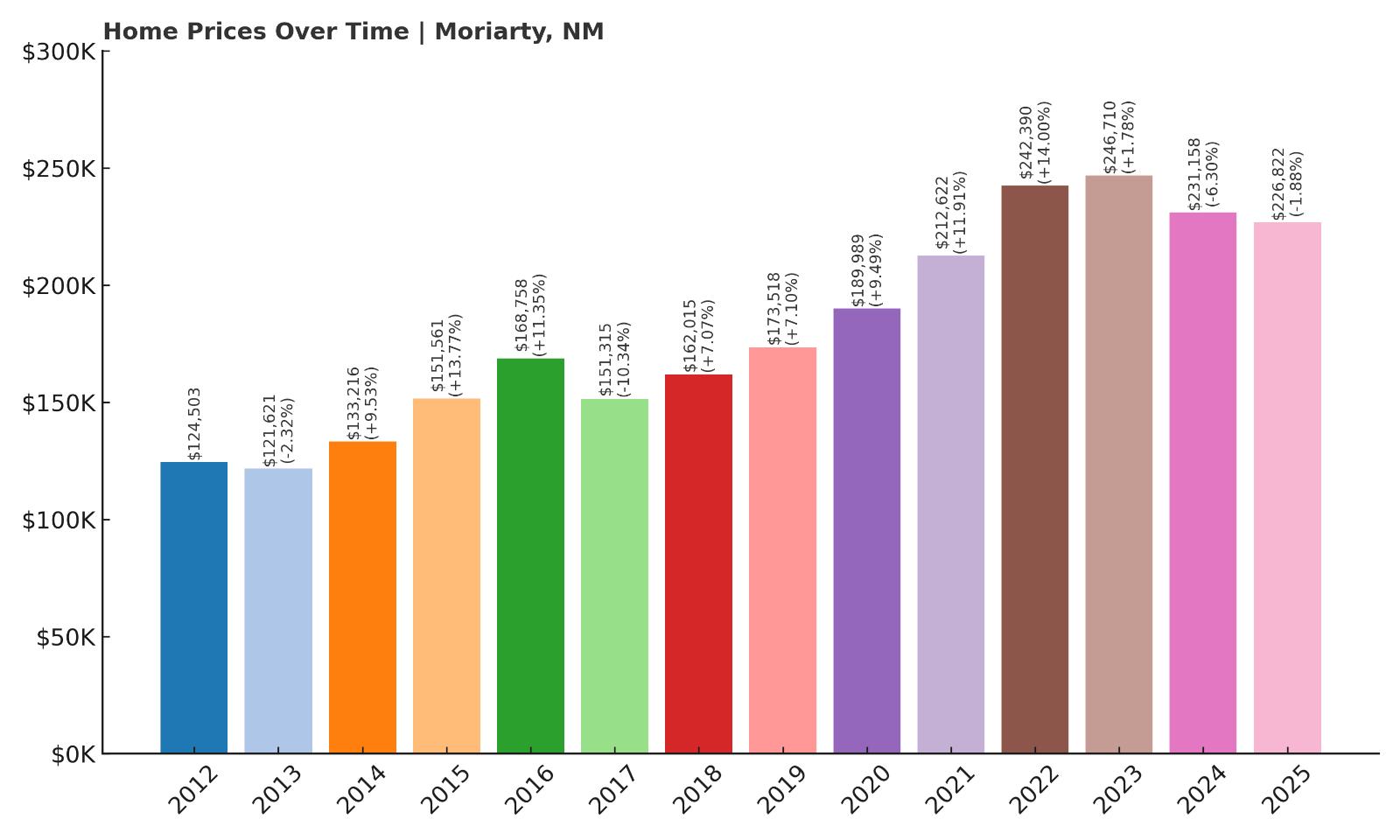

16. Moriarty – Crash Risk Percentage: 57.85%

- Crash Risk Percentage: 57.85%

- Historical crashes (8%+ drops): 2

- Worst historical crash: -10.3% (2017)

- Total price increase since 2012: 86.5%

- Overextended above long-term average: 25.2%

- Price volatility (annual swings): 8.0%

- Current 2025 price: $226,822

Moriarty has experienced two major price crashes in recent years, including a severe 10.3% drop in 2017, demonstrating the market’s tendency toward sudden corrections. Home values have surged 86% since 2012, pushing prices 25% above sustainable levels. Recent volatility continues as prices dropped 6.3% in 2024 before declining further in 2025, suggesting the market may already be entering correction territory.

Moriarty – Multiple Crashes Signal Chronic Instability

Situated along Interstate 40 between Albuquerque and Santa Fe, Moriarty has positioned itself as a bedroom community for workers in both metropolitan areas. However, this Torrance County town’s housing market has proven remarkably unstable, with significant crashes in both 2017 and recent declines that began in 2024. The 2017 crash saw prices plummet from $168,758 to $151,315, a devastating 10.3% drop that eliminated years of appreciation.

The current market shows troubling similarities to pre-crash conditions, with homes priced 25% above their long-term average despite recent declines. After peaking at $246,710 in 2023, prices have fallen for two consecutive years, dropping to $226,822 in 2025. This pattern of peaks followed by sustained declines, combined with Moriarty’s history of significant crashes, suggests the market may be entering another major correction phase that could see much steeper drops ahead.

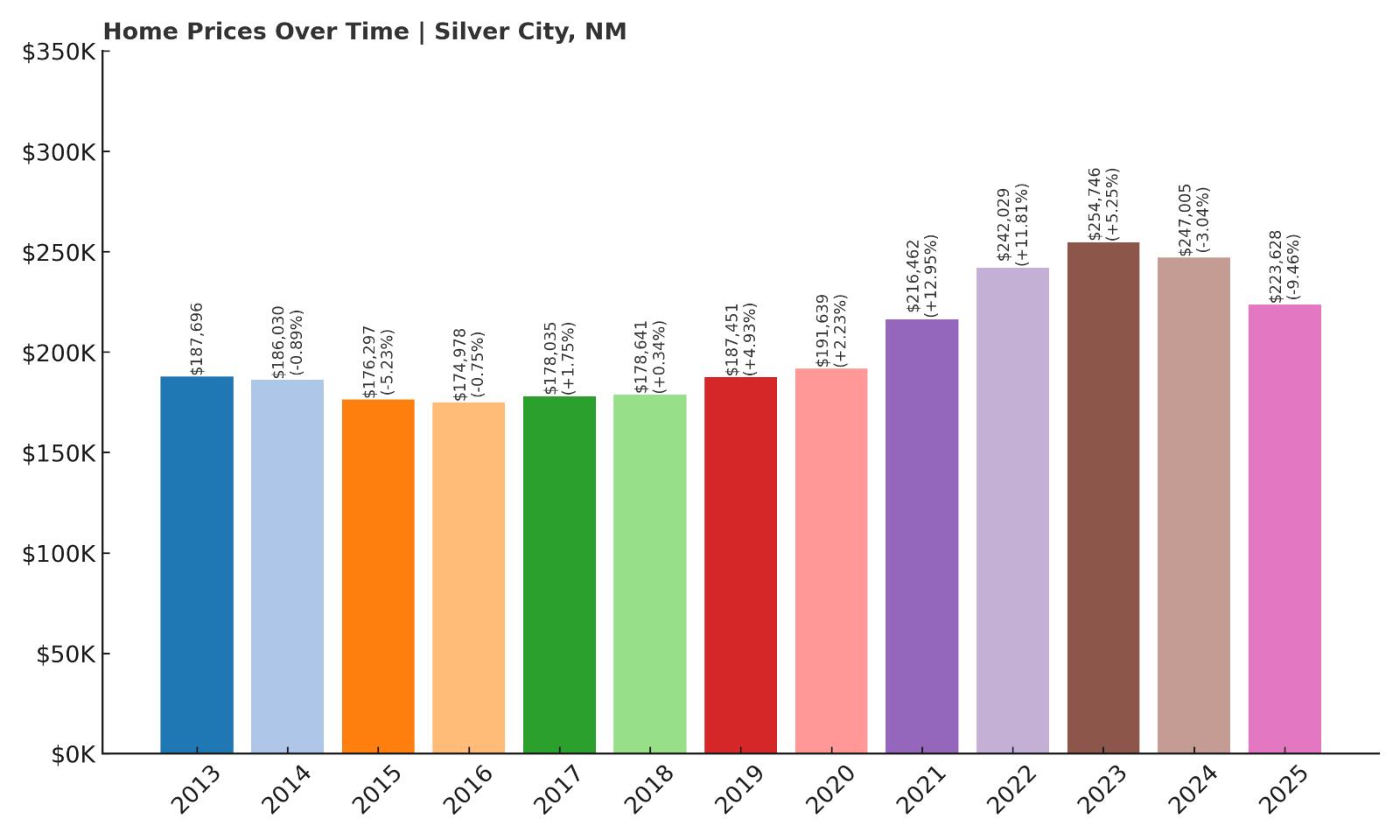

15. Silver City – Crash Risk Percentage: 57.95%

- Crash Risk Percentage: 57.95%

- Historical crashes (8%+ drops): 2

- Worst historical crash: -9.5% (2025)

- Total price increase since 2013: 27.8%

- Overextended above long-term average: 9.9%

- Price volatility (annual swings): 6.5%

- Current 2025 price: $223,628

Silver City is currently experiencing a significant price crash with a 9.5% drop in 2025, marking its worst historical decline. Despite relatively modest overextension at 9.9% above trend, the market shows vulnerability through recent volatility and a pattern of correction following peaks. The ongoing crash suggests deeper problems in this Grant County market.

Silver City – Crash Currently Underway

This historic mining town in Grant County, home to Western New Mexico University, is experiencing real-time market distress with a 9.5% price crash already underway in 2025. Home values dropped from $247,005 to $223,628, representing the steepest single-year decline in the town’s recorded history. The crash follows a period of steady appreciation that peaked in 2023 at $254,746, suggesting the market had reached unsustainable levels.

Silver City’s economy relies heavily on the university, tourism, and some remaining mining activity, creating vulnerability to economic downturns that affect these sectors. The current crash demonstrates how quickly even modestly overextended markets can correct when conditions shift. With the crash already reducing values by nearly $24,000 in a single year, homeowners face the reality that further declines may follow, particularly if underlying economic conditions deteriorate or if the university experiences enrollment challenges.

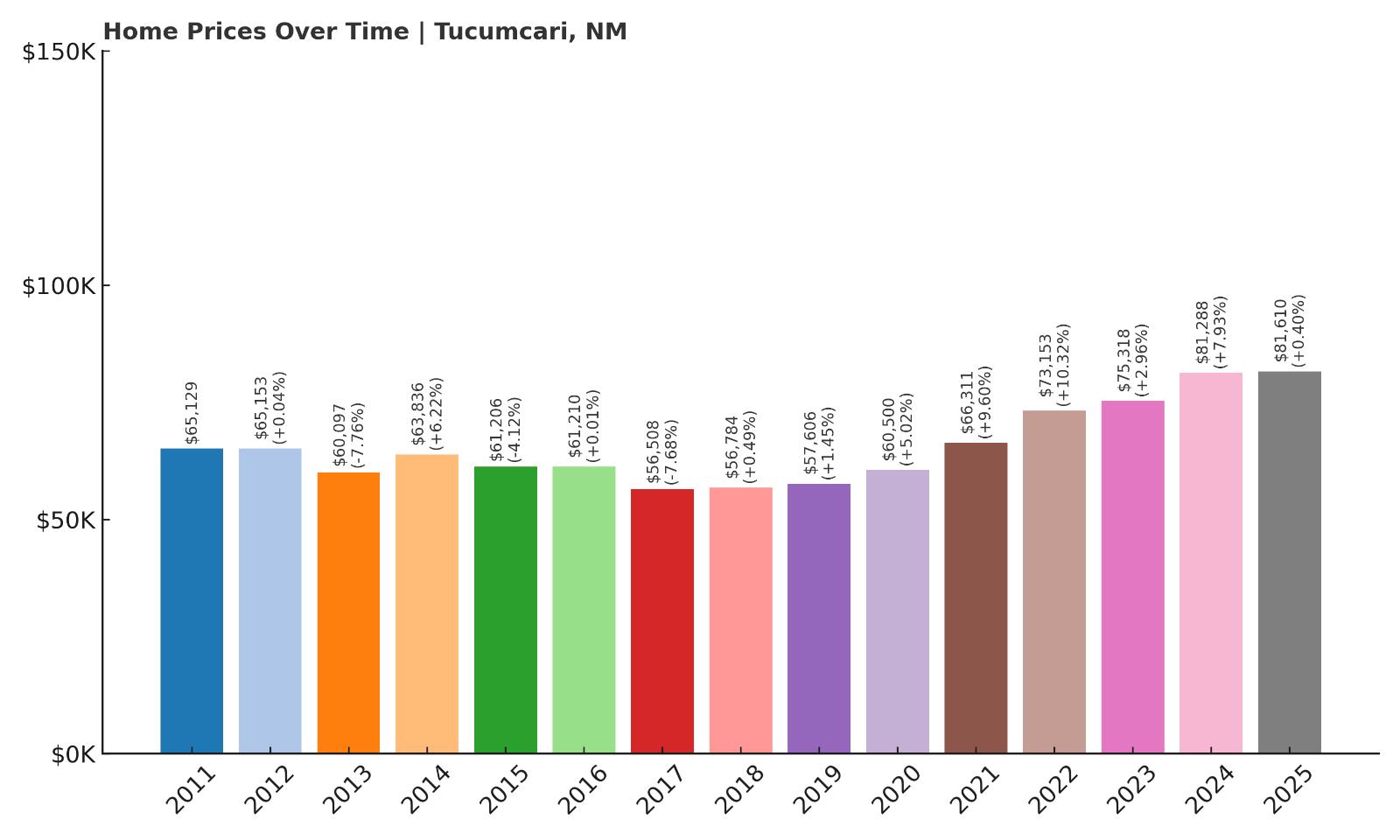

14. Tucumcari – Crash Risk Percentage: 58.05%

- Crash Risk Percentage: 58.05%

- Historical crashes (8%+ drops): 2

- Worst historical crash: -7.8% (2013)

- Total price increase since 2011: 44.4%

- Overextended above long-term average: 24.2%

- Price volatility (annual swings): 5.7%

- Current 2025 price: $81,610

Tucumcari shows persistent overvaluation with homes priced 24% above long-term trends despite multiple historical crashes. The market has experienced two significant drops, including a 7.8% decline in 2013, yet continues to maintain elevated prices. With modest growth momentum and continued overextension, another correction appears likely.

Tucumcari – Overextended Despite Low Absolute Prices

Located along historic Route 66 in Quay County, Tucumcari has built its economy around tourism and agriculture, creating a market vulnerable to external economic pressures. Despite having some of the lowest absolute home prices in the state at $81,610, the market remains mathematically overextended at 24% above its sustainable trend line. This overvaluation becomes more concerning when considering the town’s history of price crashes, including the 7.8% drop in 2013 during the broader economic recovery.

The town’s remote location and dependence on tourism make it particularly susceptible to economic downturns that reduce travel and spending. While prices have grown steadily since the 2013 crash, the 44% increase from the 2011 base has pushed values beyond what local economic fundamentals can support. Tucumcari’s combination of geographic isolation, limited economic diversity, and current overvaluation creates conditions where even small economic shocks could trigger significant price corrections.

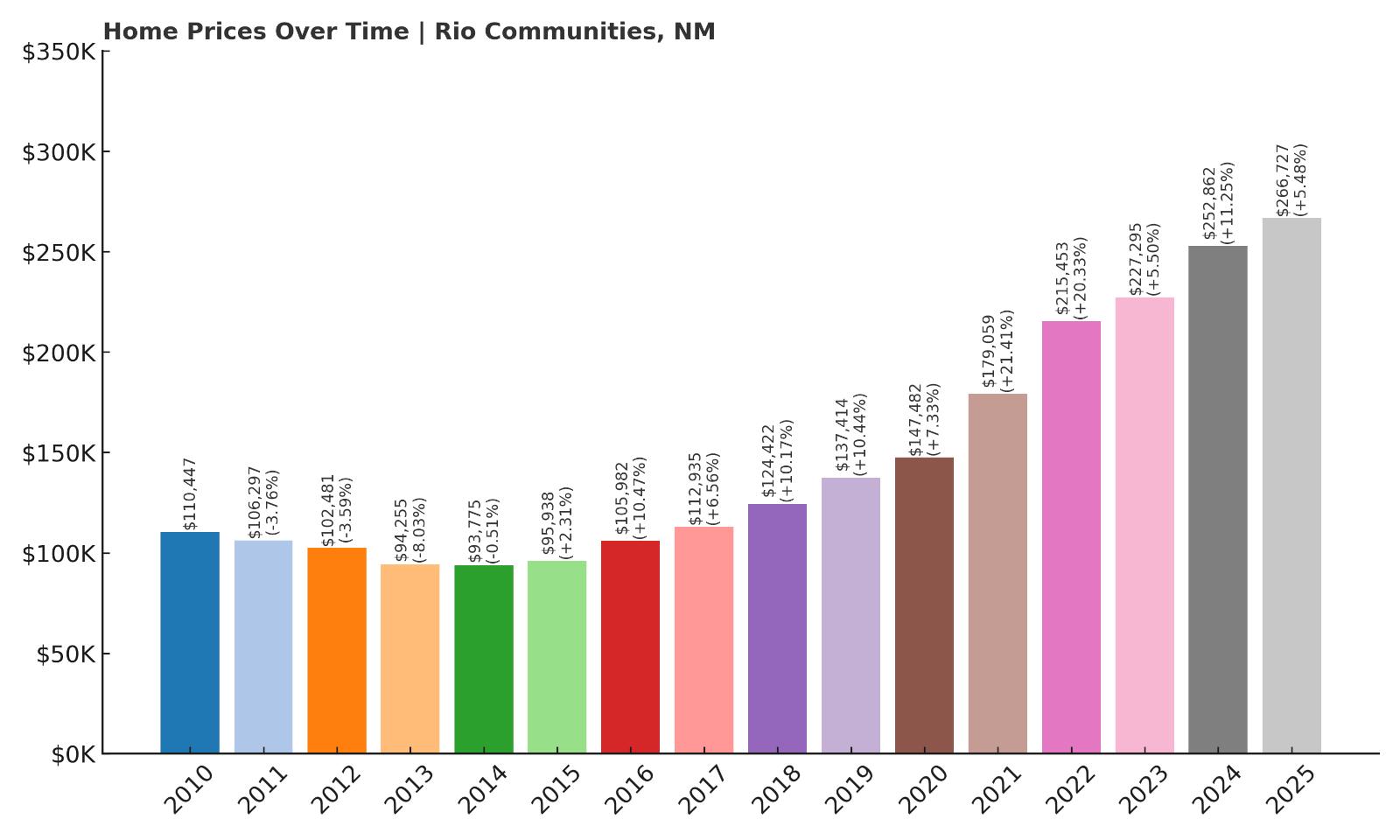

13. Rio Communities – Crash Risk Percentage: 58.55%

- Crash Risk Percentage: 58.55%

- Historical crashes (8%+ drops): 1

- Worst historical crash: -8.0% (2013)

- Total price increase since 2010: 184.4%

- Overextended above long-term average: 79.9%

- Price volatility (annual swings): 8.3%

- Current 2025 price: $266,727

Rio Communities presents one of the most dangerous overextension scenarios in New Mexico, with home values sitting nearly 80% above long-term averages after a massive 184% price increase since 2010. The community experienced an 8% crash in 2013 and shows continued volatility with annual swings of 8.3%. This extreme overvaluation creates conditions ripe for a severe correction.

Rio Communities – Extreme Overvaluation Signals Major Risk

This unincorporated community in Valencia County, situated between Albuquerque and Socorro, has experienced perhaps the most dramatic price appreciation in the state, with home values nearly tripling from $110,447 in 2010 to $266,727 today. The 184% increase has pushed the market to dangerous extremes, with current prices sitting nearly 80% above mathematically sustainable levels. This represents one of the most overextended housing markets in New Mexico, creating conditions similar to bubble markets that historically experience severe corrections.

The community’s proximity to Albuquerque has driven much of the appreciation as buyers sought more affordable alternatives to the metropolitan area. However, the 8% crash in 2013 demonstrated the market’s vulnerability to rapid corrections, and current conditions suggest a much more severe downturn could be approaching. With prices this far above sustainable levels, even a modest economic shock or shift in buyer preferences could trigger a crash that wipes out years of gains and leaves homeowners significantly underwater on their mortgages.

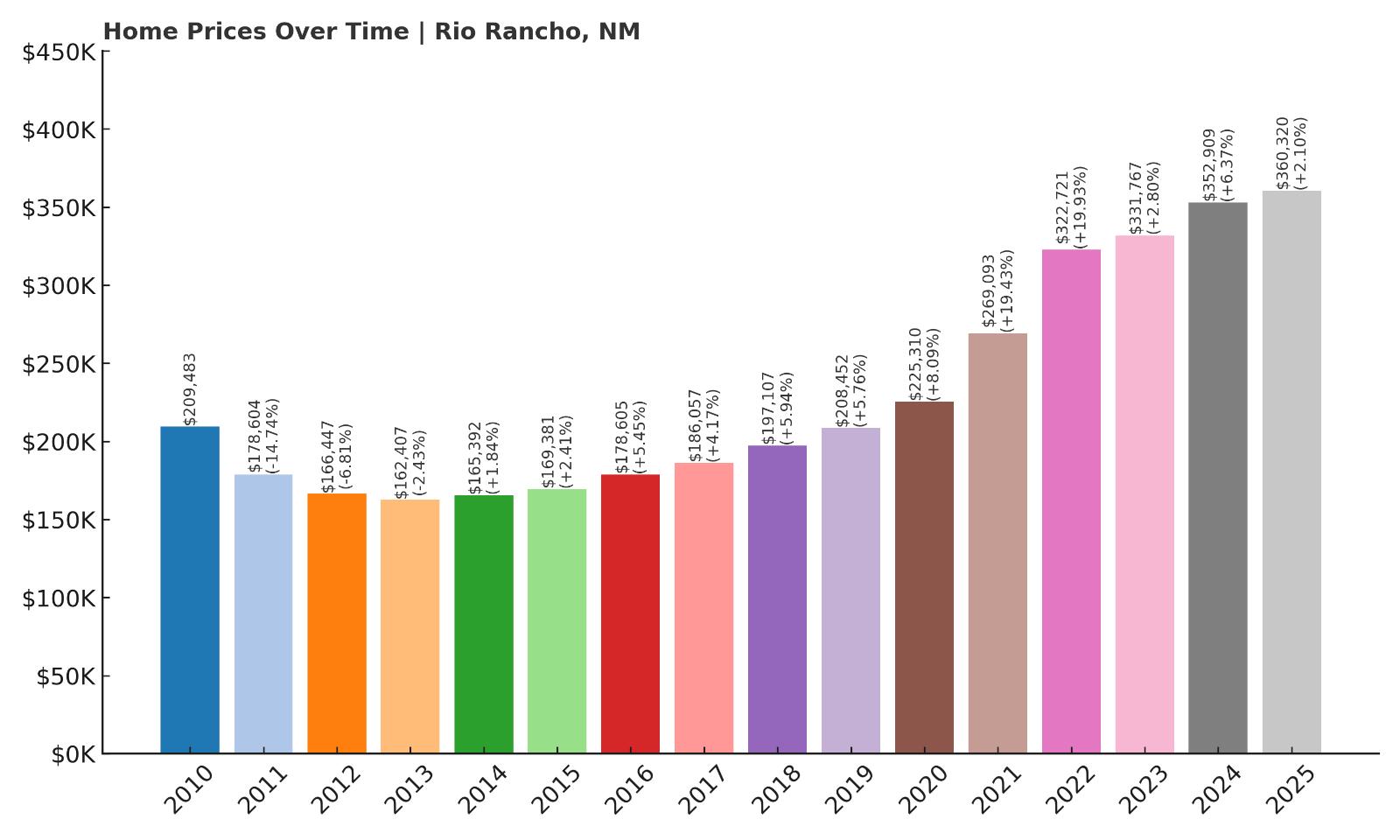

12. Rio Rancho – Crash Risk Percentage: 60.40%

- Crash Risk Percentage: 60.40%

- Historical crashes (8%+ drops): 2

- Worst historical crash: -14.7% (2011)

- Total price increase since 2010: 121.9%

- Overextended above long-term average: 56.5%

- Price volatility (annual swings): 8.6%

- Current 2025 price: $360,320

Rio Rancho, despite being one of New Mexico’s largest cities, shows severe crash risk with a history of major price drops including a devastating 14.7% decline in 2011. Home values have more than doubled since 2010 but remain dangerously overextended at 56% above sustainable levels. The combination of high absolute prices and proven crash susceptibility creates significant downside risk.

Rio Rancho – Large City With Major Crash History

As New Mexico’s third-largest city and a major suburb of Albuquerque, Rio Rancho’s housing market carries particular significance due to its size and influence on the broader metropolitan area. The city experienced a brutal 14.7% crash in 2011, wiping out over $30,000 in home values as prices plummeted from $209,483 to $178,604. This crash demonstrated that even large, established markets can experience rapid and severe corrections when economic conditions deteriorate.

Current conditions show troubling similarities to the pre-crash period, with home values at $360,320 representing a 122% increase since the 2010 baseline. Prices now sit 56% above their long-term sustainable trend, creating mathematical pressures that typically resolve through significant corrections. Rio Rancho’s proven ability to crash severely, combined with current extreme overvaluation and high absolute price levels, makes it one of the most dangerous markets for potential homebuyers who could face substantial losses if another correction occurs.

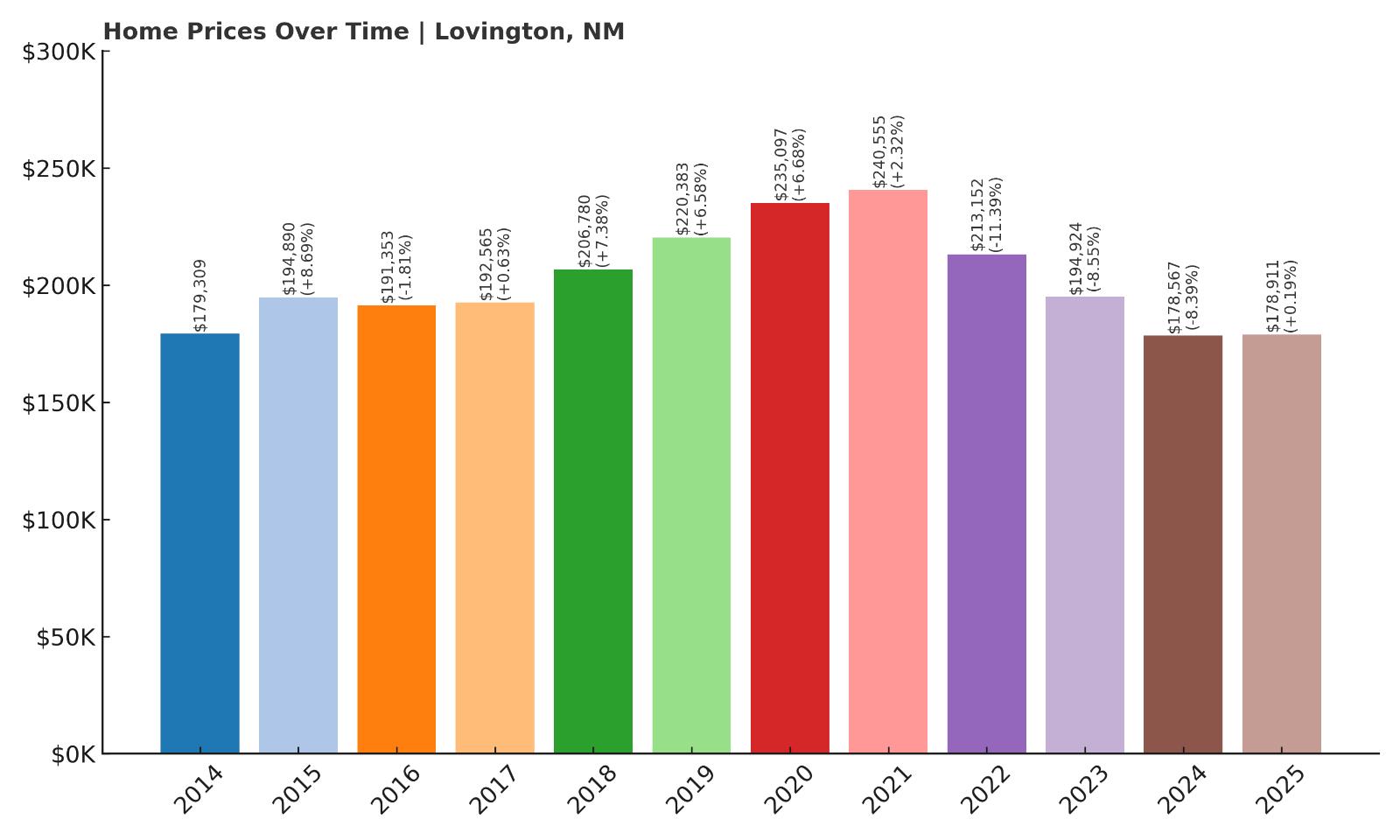

11. Lovington – Crash Risk Percentage: 60.85%

- Crash Risk Percentage: 60.85%

- Historical crashes (8%+ drops): 3

- Worst historical crash: -11.4% (2022)

- Total price increase since 2014: 0.2%

- Overextended above long-term average: -11.5%

- Price volatility (annual swings): 7.1%

- Current 2025 price: $178,911

Lovington stands out as a chronic crash market with three major price drops, including an 11.4% decline as recently as 2022. Despite being 11.5% below long-term averages, the market shows extreme instability with essentially no growth since 2014. The repeated crashes and ongoing volatility suggest fundamental market dysfunction that could trigger additional severe corrections.

Lovington – Serial Crash Pattern Indicates Deep Problems

This Lea County oil town has experienced more housing market crashes than any other community in our analysis, with three separate drops of 8% or more demonstrating chronic instability tied to energy sector volatility. The most recent crash in 2022 saw prices plummet 11.4% from $240,555 to $213,152, followed by continued declines that have persisted through 2025. Despite having essentially no price appreciation since 2014, the market continues to show signs of stress and vulnerability.

Lovington’s economy depends heavily on oil and gas production, creating boom-and-bust cycles that directly impact housing demand and prices. The town’s pattern of repeated crashes reflects this underlying economic instability, with each energy sector downturn triggering significant residential price corrections. Even though current prices sit below long-term trends, the market’s proven tendency to crash repeatedly means homeowners face ongoing risk of further declines, particularly if energy markets weaken or if the local economy fails to diversify beyond fossil fuel dependence.

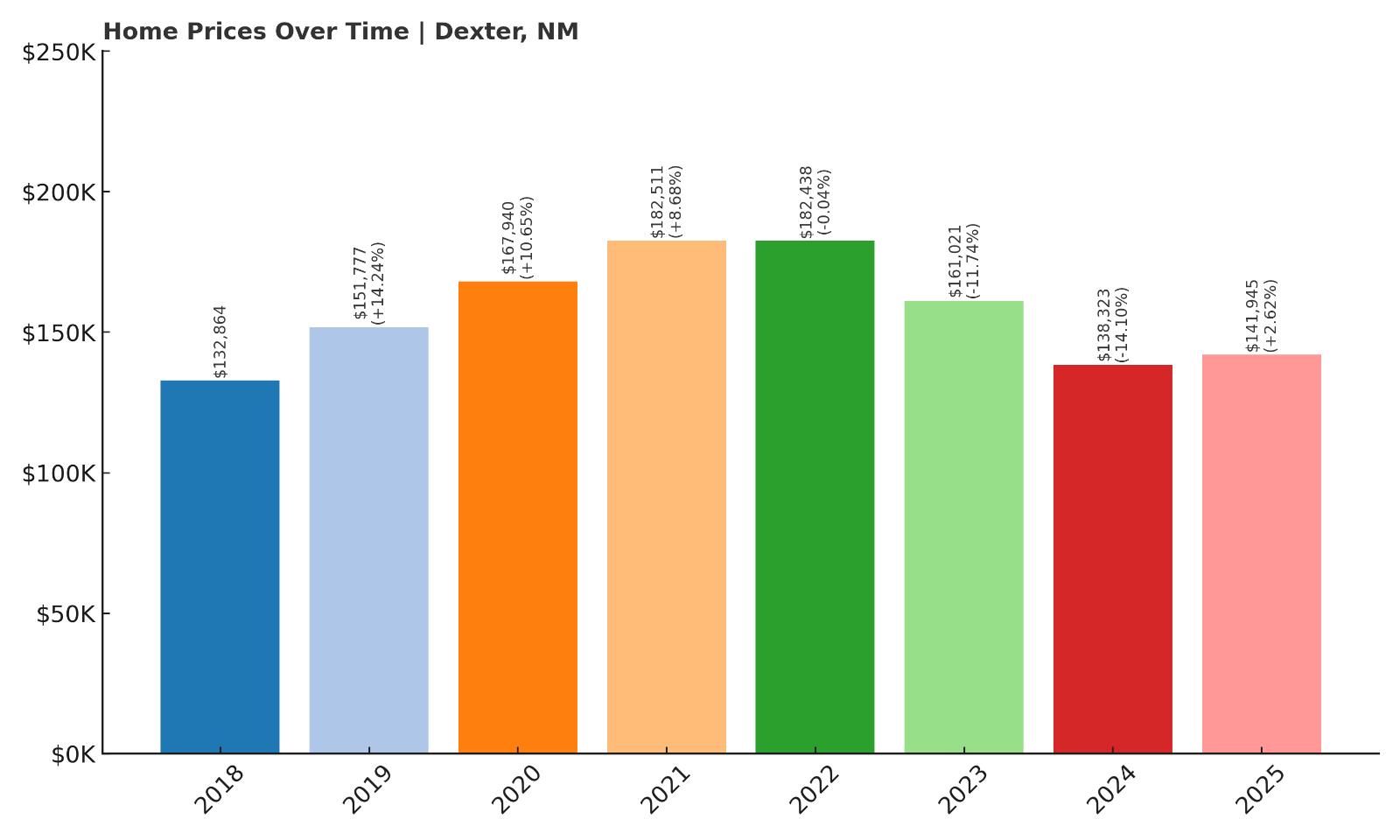

10. Dexter – Crash Risk Percentage: 61.05%

- Crash Risk Percentage: 61.05%

- Historical crashes (8%+ drops): 2

- Worst historical crash: -14.1% (2024)

- Total price increase since 2018: 6.8%

- Overextended above long-term average: -9.8%

- Price volatility (annual swings): 11.0%

- Current 2025 price: $141,945

Dexter recently experienced its worst crash on record with a devastating 14.1% drop in 2024, demonstrating severe market instability. Despite being below long-term averages, the market shows extreme volatility with annual swings of 11%. The recent crash and continued high volatility suggest ongoing fundamental problems that could produce additional sharp declines.

Dexter – Fresh Crash Wounds Still Bleeding

This small Chaves County town is still reeling from a catastrophic 14.1% housing crash in 2024 that destroyed over $22,000 in home values, dropping prices from $161,021 to $138,323. The crash represents the worst single-year decline in the community’s recorded history and demonstrates how quickly small-town markets can collapse when conditions deteriorate. Despite a modest recovery to $141,945 in 2025, the market remains deeply unstable with volatility levels of 11% that far exceed healthy norms.

Dexter’s agricultural economy and small population make it particularly vulnerable to economic shocks that can trigger rapid price corrections. The recent crash followed years of declining values that began in 2023, suggesting underlying fundamental problems rather than a temporary market adjustment. With the market still showing extreme volatility and limited economic diversity to support recovery, Dexter faces continued risk of additional crashes that could push prices even lower and trap homeowners in a cycle of declining values.

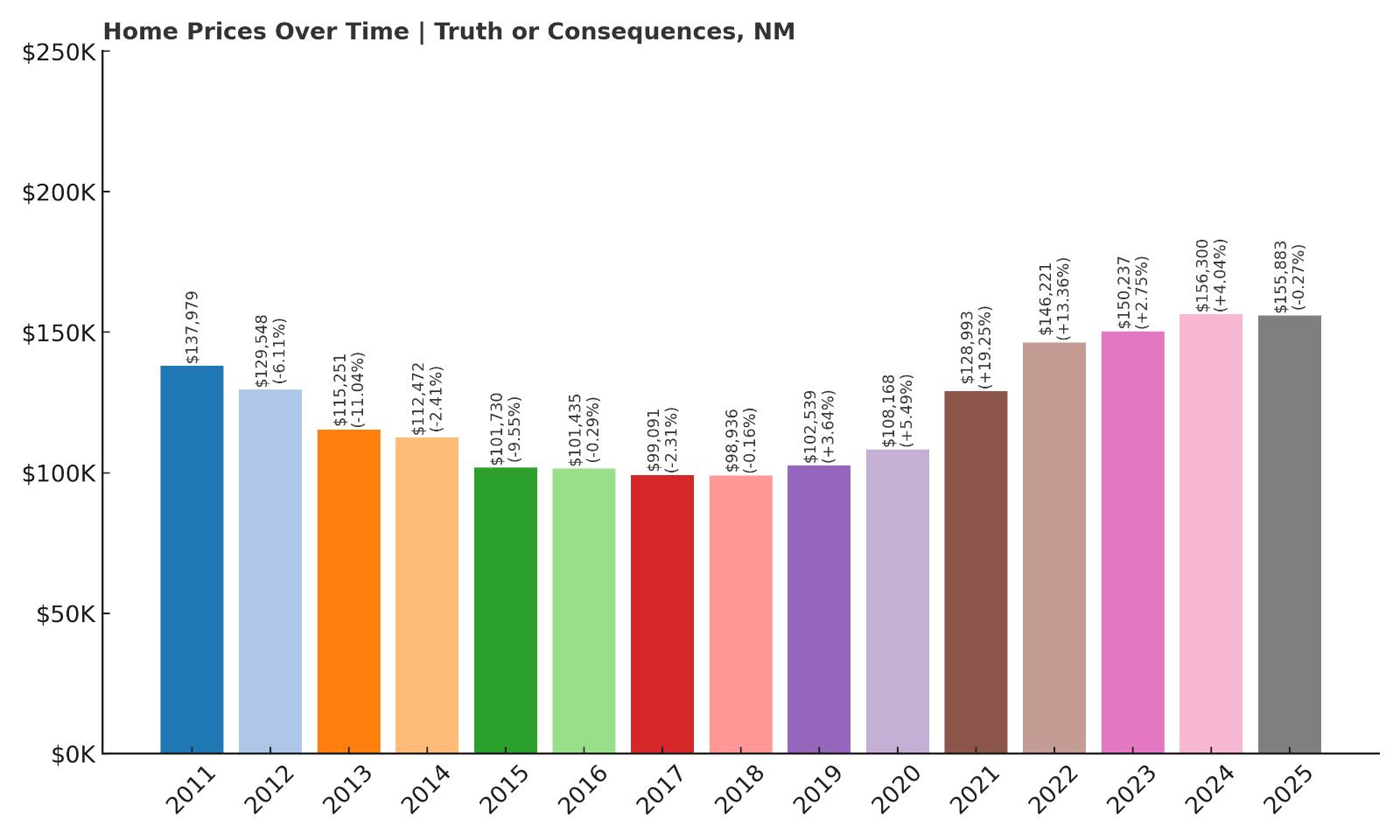

9. Truth or Consequences – Crash Risk Percentage: 63.55%

- Crash Risk Percentage: 63.55%

- Historical crashes (8%+ drops): 3

- Worst historical crash: -11.0% (2013)

- Total price increase since 2011: 57.6%

- Overextended above long-term average: 26.7%

- Price volatility (annual swings): 8.1%

- Current 2025 price: $155,883

Truth or Consequences has crashed three separate times, including an 11% decline in 2013, establishing a clear pattern of market instability. Home values remain 26.7% above sustainable levels despite the crash history, and annual volatility of 8.1% suggests continued uncertainty. The combination of repeated crashes and ongoing overextension creates high probability for another significant correction.

Truth or Consequences – Three-Time Crash Survivor Still Overextended

This Sierra County town along the Rio Grande has earned an unfortunate reputation for housing market instability, experiencing three separate crashes that demonstrate chronic vulnerability to economic disruptions. The worst crash in 2013 saw prices plummet 11% from $129,548 to $115,251, part of a broader pattern of boom-and-bust cycles that have characterized the market for over a decade. Despite this history of severe corrections, current home values at $155,883 still sit 26.7% above mathematically sustainable levels.

The town’s economy relies heavily on tourism, retiree migration, and small-scale services, creating vulnerability to external economic pressures that have repeatedly triggered housing crashes. Truth or Consequences’ pattern of recovering from crashes only to become overextended again suggests a market that fails to learn from past corrections. With prices once again stretched beyond sustainable levels and a proven track record of severe crashes, the town appears poised for another significant downturn that could devastate property values and leave homeowners facing substantial losses.

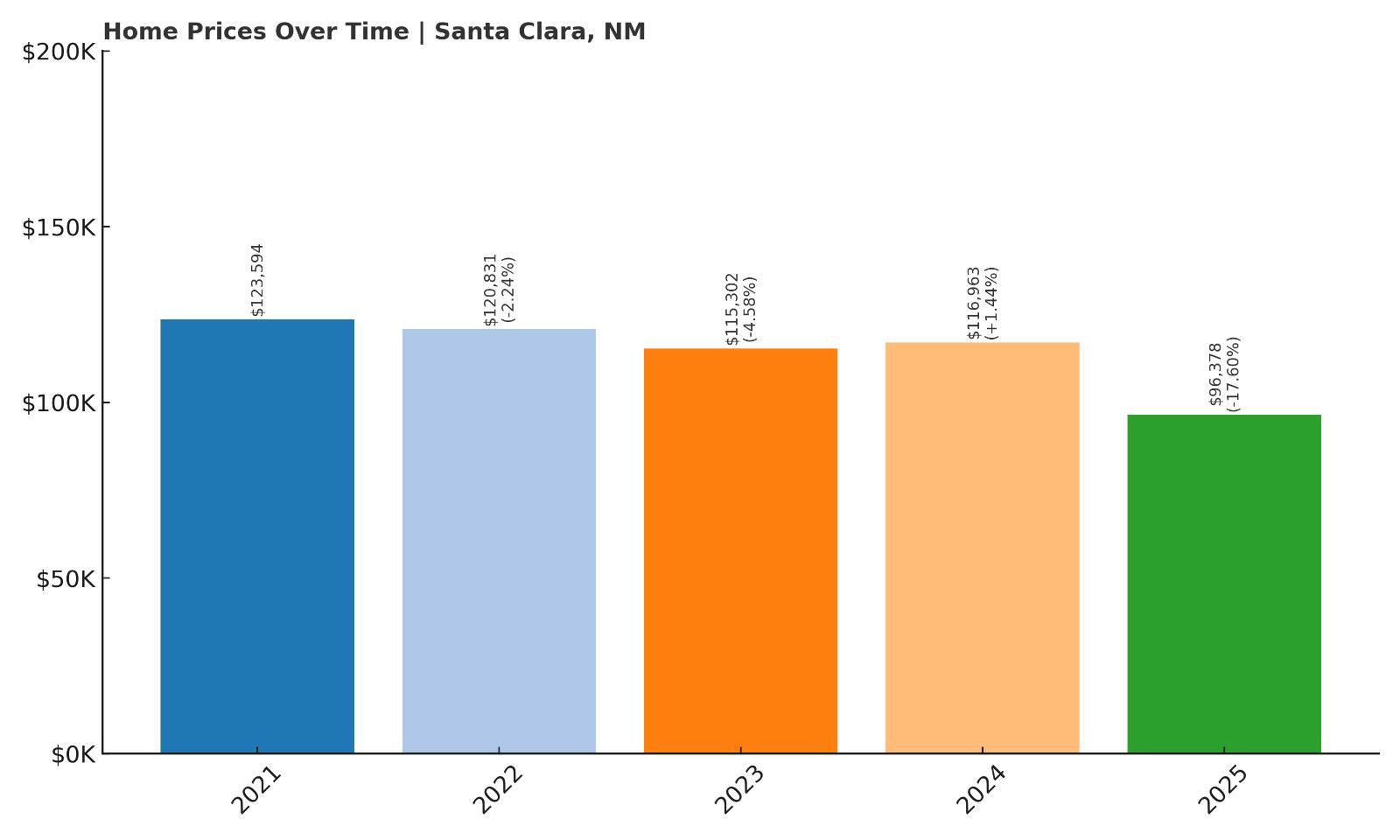

8. Santa Clara – Crash Risk Percentage: 64.40%

- Crash Risk Percentage: 64.40%

- Historical crashes (8%+ drops): 1

- Worst historical crash: -17.6% (2025)

- Total price increase since 2021: 0.0%

- Overextended above long-term average: -15.9%

- Price volatility (annual swings): 8.3%

- Current 2025 price: $96,378

Santa Clara is experiencing a catastrophic crash in real-time with a devastating 17.6% price drop in 2025, the worst in its recorded history. The crash has pushed values well below long-term averages and eliminated all price gains since 2021. The severity of the ongoing correction demonstrates how quickly small markets can collapse.

Santa Clara – Catastrophic Crash Currently Devastating Market

This small Grant County community is experiencing one of the most severe housing crashes documented in our analysis, with a catastrophic 17.6% price drop in 2025 that has destroyed over $20,000 in home values. Prices collapsed from $116,963 to $96,378, representing the steepest single-year decline recorded in the town’s history and wiping out all appreciation gains made since 2021. The crash demonstrates how quickly small, isolated markets can experience complete value destruction when economic conditions shift.

Santa Clara’s tiny population and limited economic base make it extremely vulnerable to shocks that can trigger rapid and severe price corrections. The ongoing crash has pushed home values 15.9% below their long-term trend, suggesting the market may have overcorrected and could face continued instability. With limited buyer demand and few economic drivers to support recovery, Santa Clara represents the extreme risk that small-town homeowners face when market conditions deteriorate, potentially leaving property owners trapped in a market with severely diminished values and limited prospects for recovery.

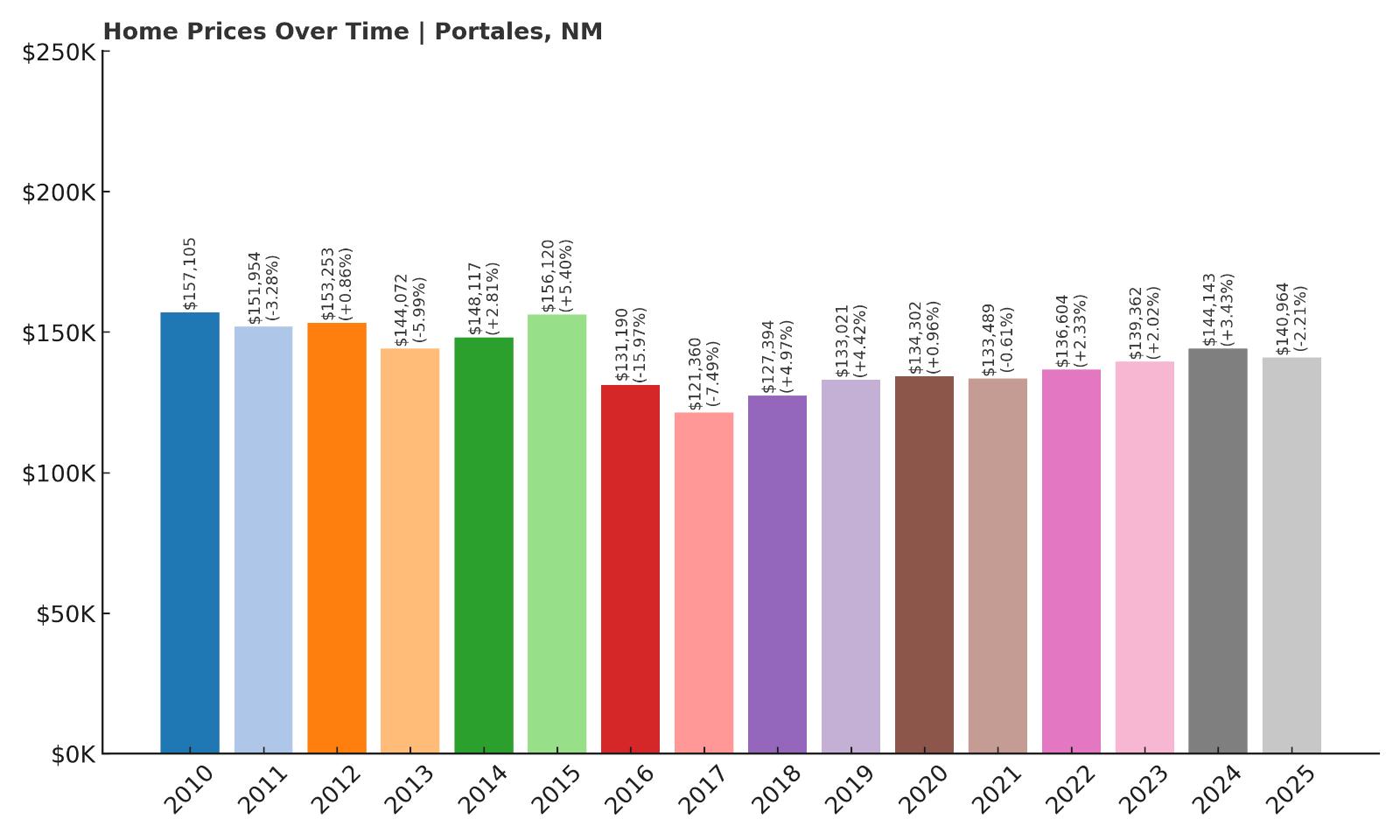

7. Portales – Crash Risk Percentage: 65.15%

- Crash Risk Percentage: 65.15%

- Historical crashes (8%+ drops): 3

- Worst historical crash: -16.0% (2016)

- Total price increase since 2010: 16.2%

- Overextended above long-term average: 0.1%

- Price volatility (annual swings): 5.7%

- Current 2025 price: $140,964

Portales has suffered three major crashes, including a devastating 16% decline in 2016 that represents one of the worst single-year drops in New Mexico. Despite being near long-term trend levels, the market’s history of severe corrections and recent declining momentum create significant downside risk. The pattern of repeated crashes suggests chronic market dysfunction.

Portales – Serial Crashes Including 16% Single-Year Devastation

Home to Eastern New Mexico University, Portales has experienced some of the most severe housing market crashes in the state, with three separate corrections including a catastrophic 16% decline in 2016 that destroyed nearly $25,000 in home values overnight. The 2016 crash dropped prices from $156,120 to $131,190, demonstrating how quickly university towns can experience market collapse when economic conditions deteriorate or enrollment patterns shift. Despite being a regional education center, the market has proven remarkably unstable over the past 15 years.

Current market conditions show troubling signs of renewed weakness, with prices declining 2.2% in 2025 after modest growth in previous years. While home values sit close to their long-term trend at $140,964, Portales’ proven ability to experience devastating crashes means even small economic disruptions could trigger another severe correction. The town’s dependence on university employment and limited economic diversity create ongoing vulnerability that has repeatedly produced major housing market disasters, making it one of the riskiest places to own property in New Mexico.

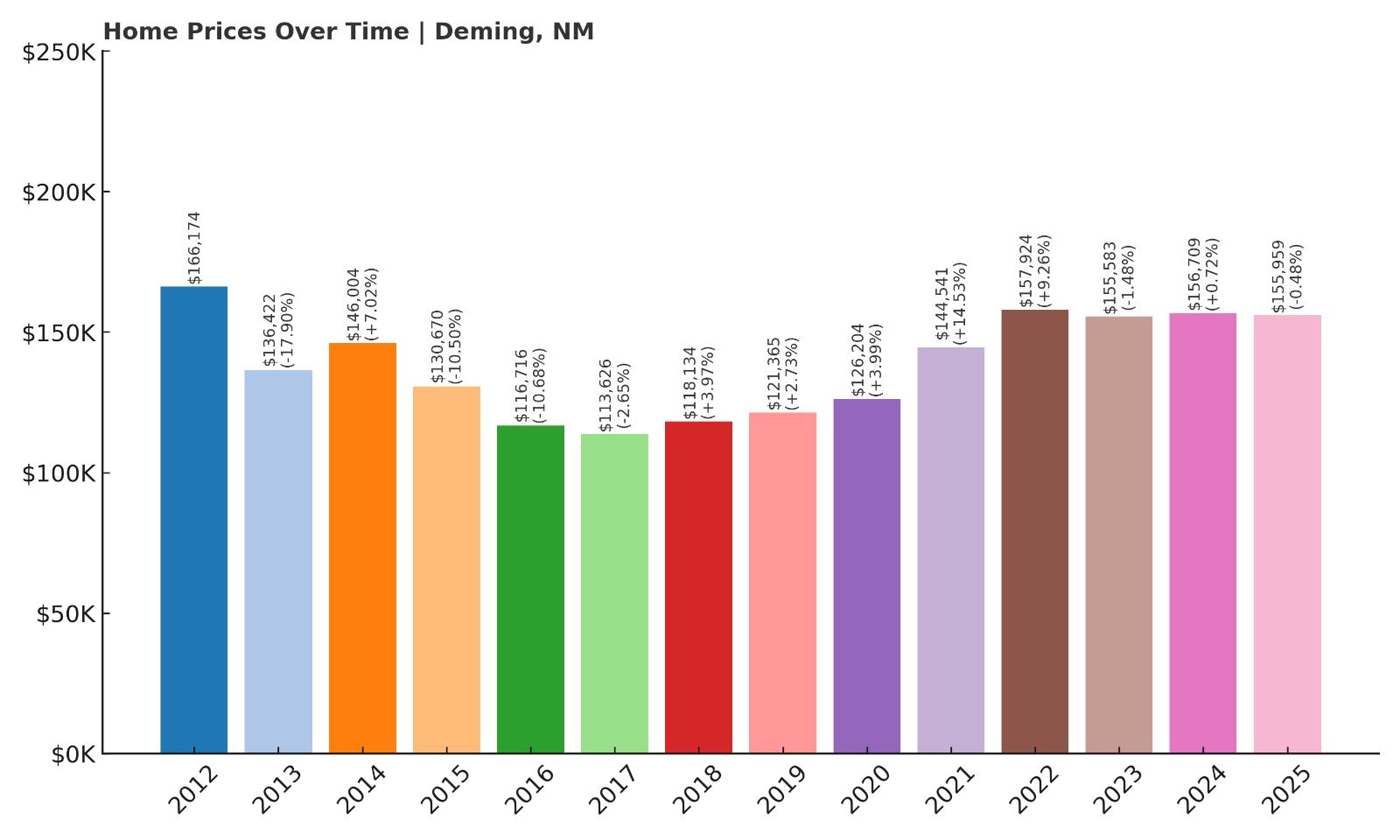

6. Deming – Crash Risk Percentage: 65.50%

- Crash Risk Percentage: 65.50%

- Historical crashes (8%+ drops): 3

- Worst historical crash: -17.9% (2013)

- Total price increase since 2012: 37.3%

- Overextended above long-term average: 12.2%

- Price volatility (annual swings): 8.9%

- Current 2025 price: $155,959

Deming holds the distinction of experiencing one of New Mexico’s worst housing crashes with a devastating 17.9% decline in 2013. The market has suffered three separate major corrections and continues to show instability with high volatility and modest overextension. Recent price weakness suggests another correction may be beginning.

Deming – Record-Breaking Crash History Continues to Haunt Market

This Luna County border town experienced one of the most devastating housing crashes in New Mexico’s recorded history when prices plummeted 17.9% in 2013, destroying nearly $30,000 in home values as the market collapsed from $166,174 to $136,422. The crash was part of a broader pattern of instability that has seen Deming experience three separate major corrections, establishing it as one of the state’s most crash-prone markets. The severity of the 2013 decline demonstrates how quickly border communities can lose value when economic conditions deteriorate.

Despite recovering from the 2013 disaster, Deming’s market continues to show signs of instability with home values declining slightly in recent years and remaining 12.2% above sustainable levels. The town’s economy relies heavily on agriculture, border trade, and some manufacturing, creating vulnerability to external economic shocks that have repeatedly triggered severe housing corrections. With a proven track record of catastrophic crashes and current signs of renewed weakness, Deming represents extreme risk for homeowners who could face another devastating correction that wipes out years of recovery gains.

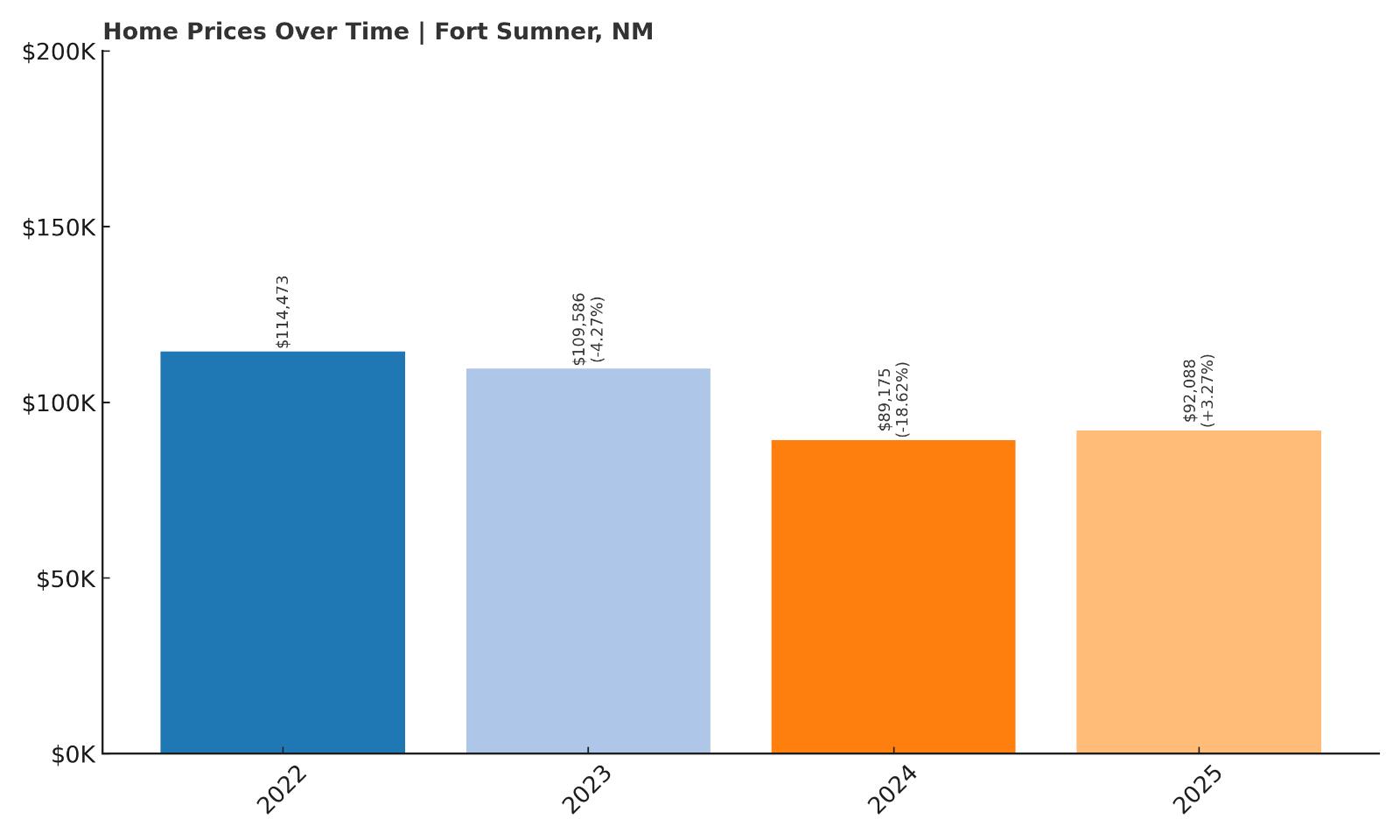

5. Fort Sumner – Crash Risk Percentage: 66.95%

- Crash Risk Percentage: 66.95%

- Historical crashes (8%+ drops): 1

- Worst historical crash: -18.6% (2024)

- Total price increase since 2022: 3.3%

- Overextended above long-term average: -9.1%

- Price volatility (annual swings): 11.1%

- Current 2025 price: $92,088

Fort Sumner recently experienced a catastrophic 18.6% crash in 2024, among the worst single-year declines recorded in New Mexico. Despite being below long-term averages, the market shows extreme volatility of 11.1% and limited growth since 2022. The recent crash and ongoing instability suggest continued vulnerability to severe corrections.

Fort Sumner – Fresh From Catastrophic 18.6% Market Collapse

This historic De Baca County town, famous as the location where Billy the Kid was killed, recently suffered one of the most devastating housing crashes in New Mexico history with an 18.6% price collapse in 2024. Home values plummeted from $109,586 to $89,175, destroying over $20,000 in property values and demonstrating how quickly small rural markets can experience complete breakdown. The crash represents the worst single-year decline recorded in the community’s recent history and has left the market deeply scarred.

Fort Sumner’s tiny population and agricultural economy make it extremely vulnerable to economic shocks that can trigger rapid and severe price corrections. Despite a modest 3.3% recovery in 2025 to $92,088, the market remains deeply unstable with volatility levels of 11.1% that indicate continued dysfunction. The recent catastrophic crash shows how small-town markets can experience complete value destruction, and with limited economic drivers and ongoing instability, Fort Sumner faces continued risk of additional crashes that could push property values even lower.

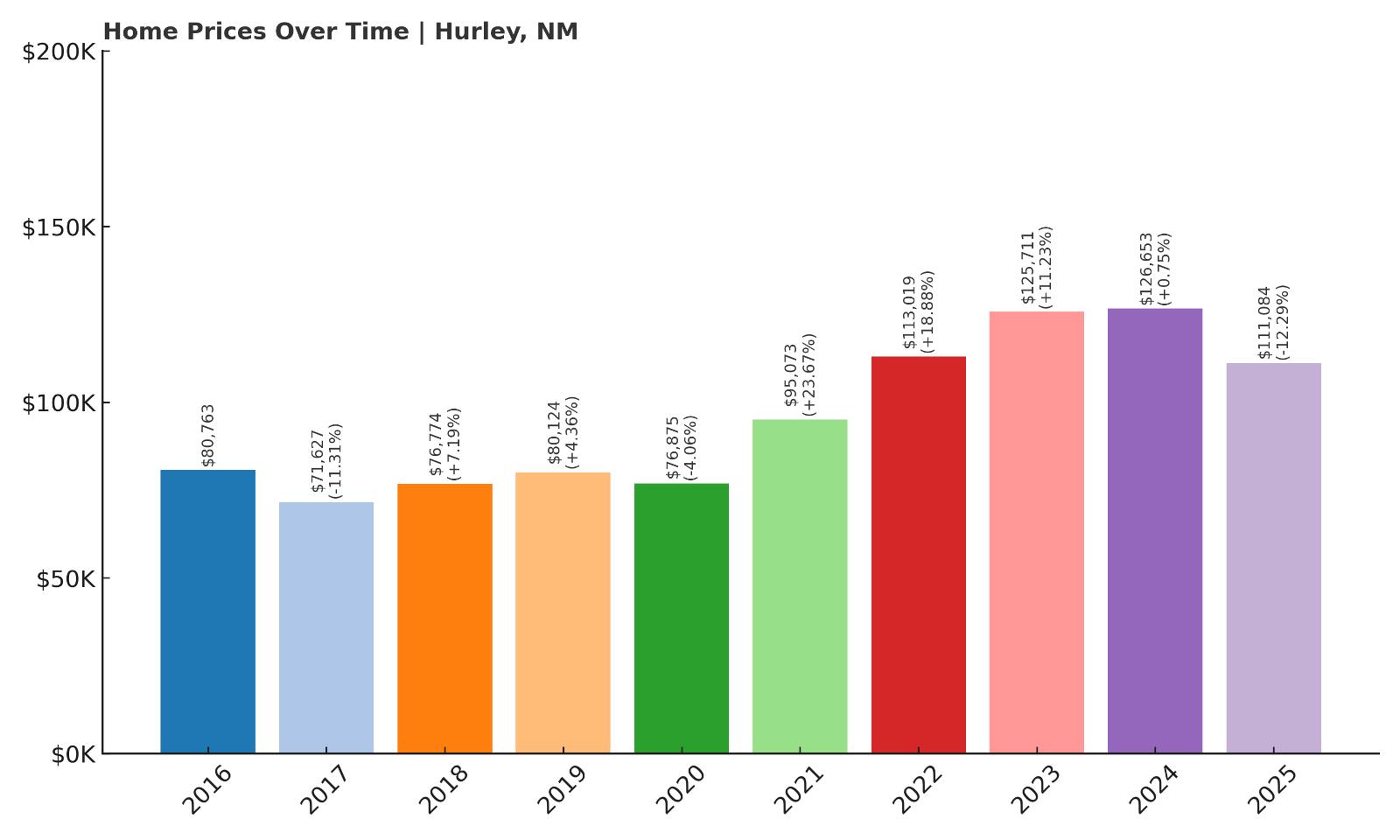

4. Hurley – Crash Risk Percentage: 68.75%

- Crash Risk Percentage: 68.75%

- Historical crashes (8%+ drops): 2

- Worst historical crash: -12.3% (2025)

- Total price increase since 2016: 55.1%

- Overextended above long-term average: 16.0%

- Price volatility (annual swings): 12.5%

- Current 2025 price: $111,084

Hurley is currently experiencing a major crash with a 12.3% decline in 2025, marking its worst historical drop. The market shows extreme volatility of 12.5% and remains overextended despite the ongoing correction. With two previous crashes and current instability, Hurley demonstrates chronic market dysfunction that threatens further severe declines.

Hurley – Crash In Progress With Extreme Volatility

This small Grant County mining town is currently experiencing a severe housing market crash with a 12.3% price decline in 2025 that has destroyed over $15,000 in home values, dropping from $126,653 to $111,084. The ongoing crash represents the worst single-year decline in Hurley’s recorded history and demonstrates the extreme volatility that characterizes this market, with annual price swings averaging 12.5%. Despite the current correction, home values remain 16% above their long-term sustainable trend, suggesting the crash may continue.

Hurley’s economy has historically depended on mining operations that create boom-and-bust cycles directly reflected in housing prices. The town has experienced two previous major crashes, establishing a pattern of chronic market instability that makes homeownership extremely risky. With the current crash still unfolding and prices remaining above sustainable levels even after the significant decline, Hurley faces the prospect of continued corrections that could drive values much lower and trap property owners in a severely depressed market with limited prospects for recovery.

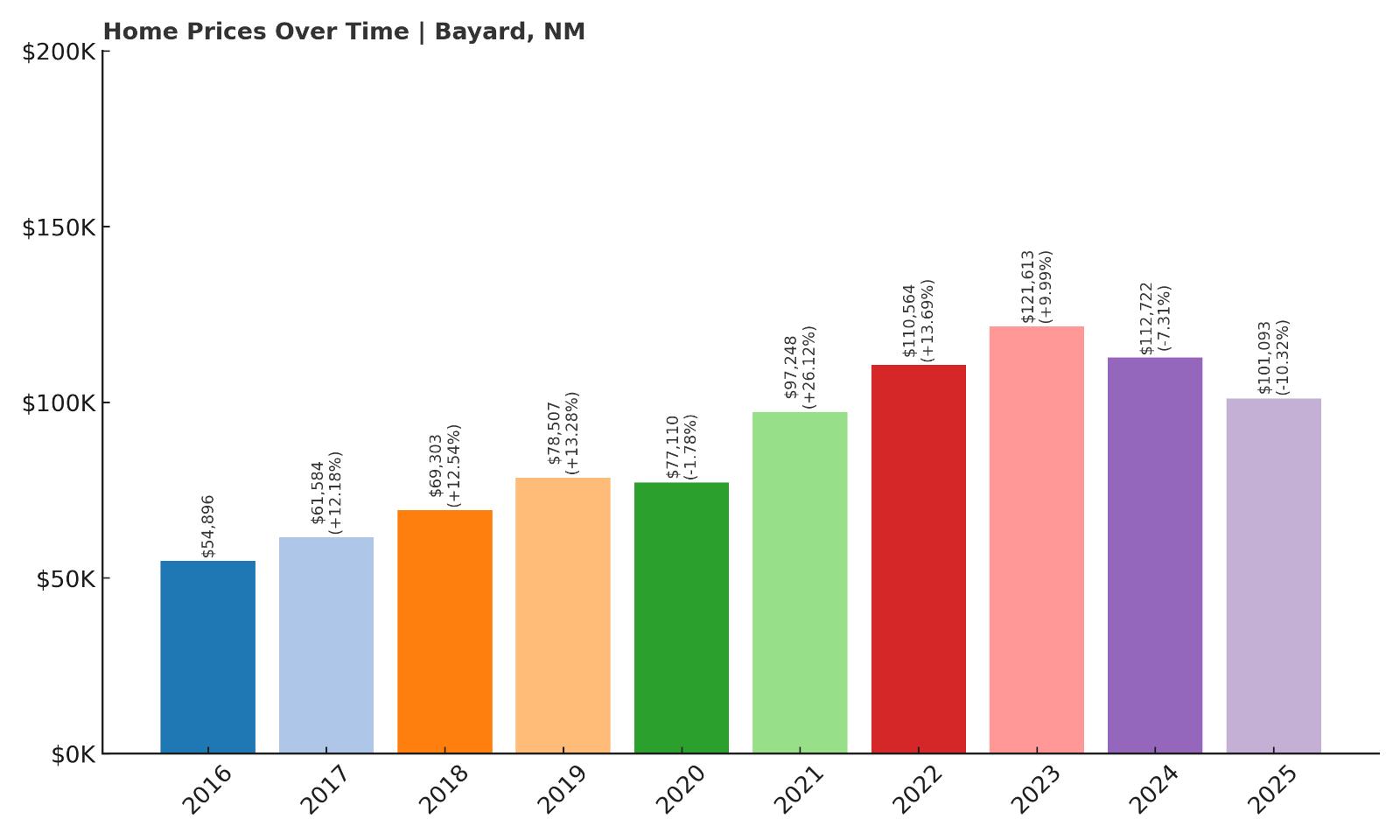

3. Bayard – Crash Risk Percentage: 77.15%

- Crash Risk Percentage: 77.15%

- Historical crashes (8%+ drops): 2

- Worst historical crash: -10.3% (2025)

- Total price increase since 2016: 84.2%

- Overextended above long-term average: 14.3%

- Price volatility (annual swings): 11.7%

- Current 2025 price: $101,093

Bayard is experiencing its worst crash on record with a 10.3% decline in 2025, following massive 84% price growth since 2016. Despite the ongoing correction, homes remain 14.3% overextended with extreme volatility of 11.7%. The current crash combined with chronic instability and continued overvaluation creates extreme risk for additional severe declines.

Bayard – Current Crash Following Massive Overextension

This tiny Grant County mining community is currently suffering through its worst housing crash on record, with a devastating 10.3% price decline in 2025 that has wiped out over $11,000 in home values, dropping from $112,722 to $101,093. The crash follows years of unsustainable appreciation that saw home values surge 84% since 2016, creating dangerous overextension that has now begun to correct. Despite the significant decline, prices remain 14.3% above mathematically sustainable levels, suggesting the crash may intensify.

Bayard’s economy depends heavily on mining operations and related services, creating extreme vulnerability to commodity price cycles and operational changes that can devastate local housing demand. The town’s tiny population and limited economic diversity amplify volatility, as evidenced by annual price swings averaging 11.7%. With the current crash already underway and prices still overextended despite the correction, Bayard faces the prospect of continued severe declines that could push property values much lower and create a prolonged period of market distress for homeowners.

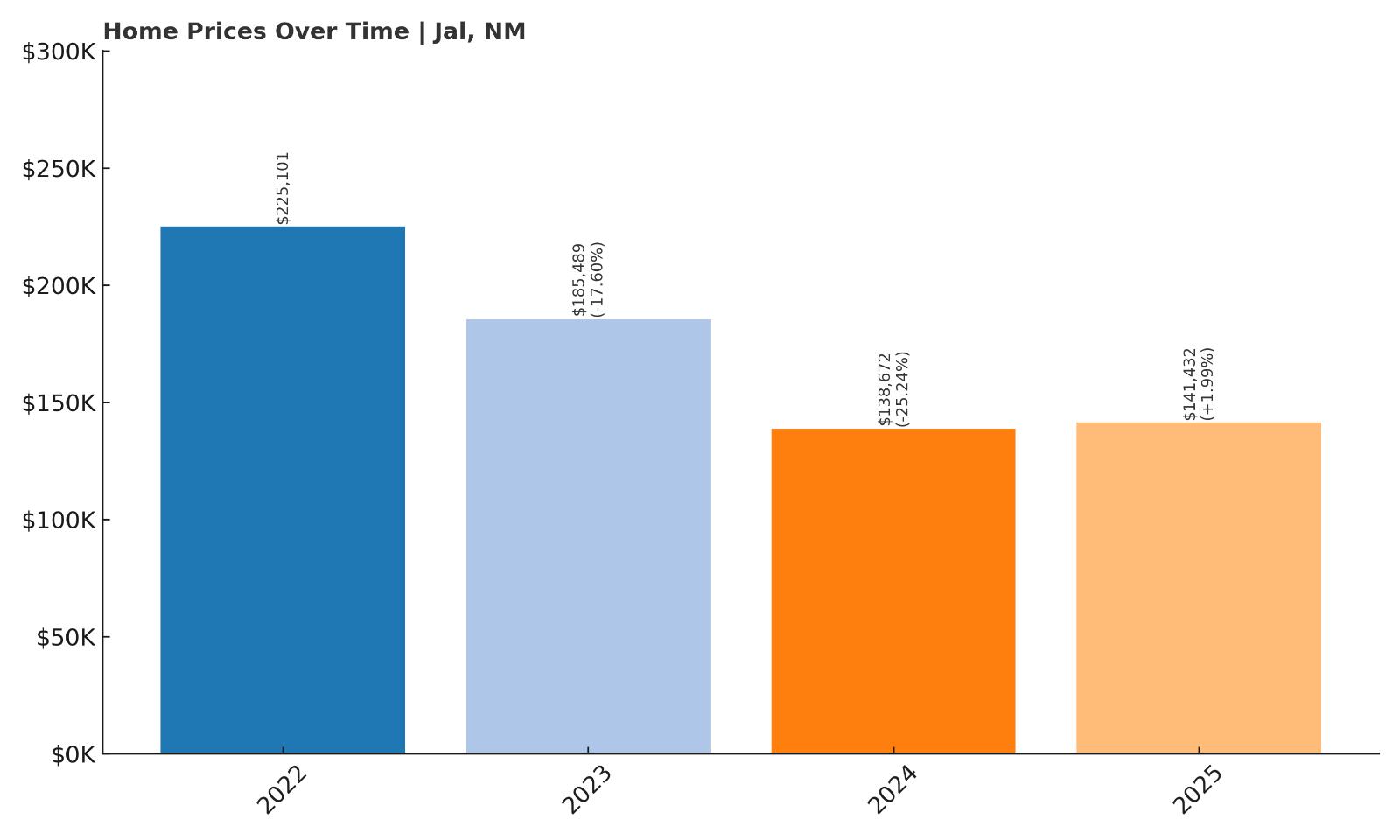

2. Jal – Crash Risk Percentage: 78.40%

- Crash Risk Percentage: 78.40%

- Historical crashes (8%+ drops): 2

- Worst historical crash: -25.2% (2024)

- Total price increase since 2022: 2.0%

- Overextended above long-term average: -18.1%

- Price volatility (annual swings): 14.0%

- Current 2025 price: $141,432

Jal experienced New Mexico’s most catastrophic housing crash with a devastating 25.2% decline in 2024, destroying nearly $47,000 in home values. Despite being well below long-term averages, the market shows extreme volatility of 14% and minimal growth since 2022. The severity of the recent crash and ongoing instability suggest potential for additional devastating corrections.

Jal – Survivor of State’s Worst Housing Crash

This Lea County oil town holds the unfortunate distinction of experiencing New Mexico’s most catastrophic housing crash, with a devastating 25.2% price collapse in 2024 that destroyed nearly $47,000 in home values as prices plummeted from $185,489 to $138,672. The crash represents the most severe single-year decline recorded in our analysis and demonstrates how quickly energy-dependent communities can experience complete market breakdown when sector conditions deteriorate. The magnitude of the crash has left lasting scars on the local housing market.

Jal’s economy depends almost entirely on oil and gas production, creating extreme vulnerability to energy price cycles and operational changes that directly impact housing demand and values. The town has experienced two major crashes, with the 2024 disaster following a previous significant decline in 2023, establishing a pattern of chronic instability. Despite modest recovery to $141,432 in 2025, the market remains deeply unstable with volatility levels of 14% that far exceed healthy norms. The combination of energy sector dependence, proven crash susceptibility, and ongoing extreme volatility makes Jal one of the most dangerous housing markets in New Mexico.

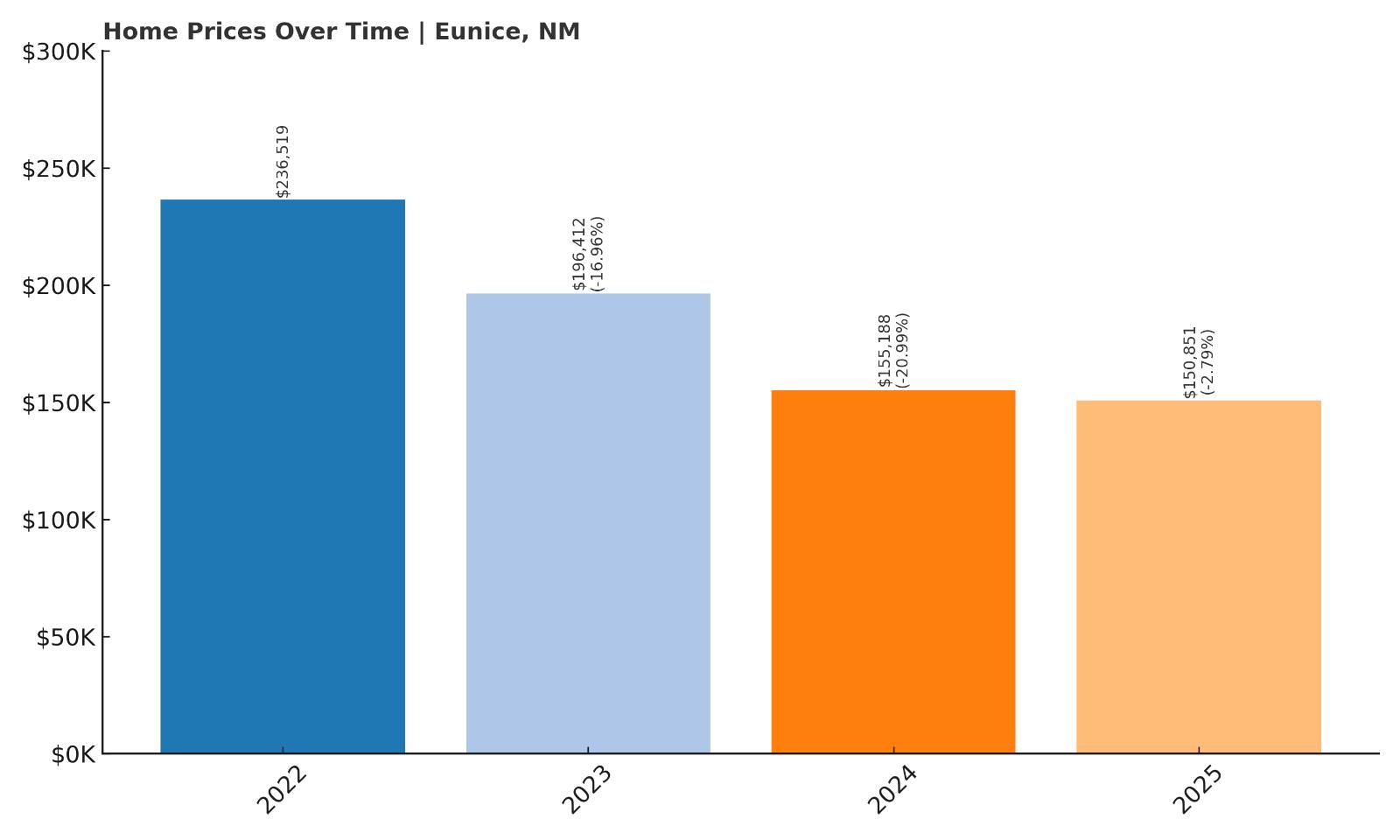

1. Eunice – Crash Risk Percentage: 81.25%

- Crash Risk Percentage: 81.25%

- Historical crashes (8%+ drops): 2

- Worst historical crash: -21.0% (2024)

- Total price increase since 2022: 0.0%

- Overextended above long-term average: -18.3%

- Price volatility (annual swings): 9.6%

- Current 2025 price: $150,851

Eunice tops our crash risk rankings after experiencing a catastrophic 21% decline in 2024, followed by continued weakness that has eliminated all gains since 2022. Despite being significantly below long-term averages, the market shows persistent instability and vulnerability. The combination of recent devastating crashes and ongoing market dysfunction creates the highest crash risk in New Mexico.

Eunice – New Mexico’s Highest Crash Risk Market

This Lea County oil town earns the dubious distinction of having New Mexico’s highest housing crash risk after experiencing a catastrophic 21% price collapse in 2024 that destroyed over $41,000 in home values, dropping from $196,412 to $155,188. The devastating crash was followed by continued declines in 2025, pushing values down to $150,851 and eliminating all appreciation gains made since 2022. The severity and persistence of the correction demonstrate fundamental market breakdown that extends beyond typical cyclical adjustments.

Eunice’s economy revolves almost entirely around oil and gas extraction, creating extreme dependence on energy sector performance that has repeatedly triggered severe housing market crashes. The town has experienced two major corrections in recent years, with the 2024 disaster representing one of the worst single-year declines recorded in New Mexico. Despite being 18.3% below long-term trend levels, the market continues to show signs of distress and instability that suggest additional crashes remain possible. The combination of energy sector volatility, proven crash susceptibility, and ongoing market dysfunction makes Eunice the most dangerous place to own real estate in New Mexico, where homeowners face extreme risk of further devastating losses.